Stocks Head For First Drop Of 2026 As Focus Turns To Geopolitics, Macro

US equity futures are weaker but off session lows, as markets pause ahead of a series of US labor and economic data. As of 8:00am ET, S&P futures are down 0.1% as global equity markets have run into some resistance after a strong start to 2026; Nasdaq futures dip 0.2% with TMT underperforming premarket, with most Mag7 and Semis names lower while Energy, Healthcare and Staples rallying pre-mkt. Bonds are bid with yields down 2-4bp as the curve flattens; the USD is unchanged. n commodities, Ags are the bright spot as we see some profit-taking in Metals and oil fell after Trump said Venezuela would turn over as many as 50 million barrels of crude to the US with sales proceeds are expected to be split between the two countries. Today's US economic calendar includes December ADP employment change (8:15am), December ISM services index, November JOLTS job openings and October factors orders (10am). Scheduled Fed speakers include Bowman on banking supervision and regulation at 4:10pm

In premarket trading, Mag 7 stocks are mostly lower (Nvidia +0.6%, Tesla +0.2%, Apple -0.2%, Alphabet -0.3%, Microsoft -0.1%, Amazon -0.2%, Meta Platforms -0.4%)

- Miners and royalty companies are down as gold and silver pull back with broader markets as traders look to upcoming US economic data later this week.

- AST SpaceMobile Inc. (ASTS) falls 6% after Scotiabank cut the recommendation on the satellite broadband company to sector underperform, saying it faces an “uphill battle” given the leadership position of Elon Musk’s Starlink.

- First Solar Inc. (FSLR) falls 4% after Jefferies cut its recommendation to hold from buy on concerns over tariffs and its valuation.

- Mobileye Global Inc. (MBLY) climbs 10% with the company to acquire Israeli startup Mentee Robotics in a cash-and-stock deal valued at $900 million, as the self-driving car system company expands its robotics capabilities.

- Monte Rosa Therapeutics (GLUE) rises 38% after the biotech announced positive interim data from an ongoing Phase 1 clinical study.

- Strategy (MSTR) climbs 4% after MSCI decided for now to keep digital asset treasury companies in its stock market indexes.

- StoneCo (STNE) falls 5% after after the Brazilian digital payments company said CEO Pedro Zinner will resign for personal reasons effective March 2026.

- Ventyx Biosciences Inc. (VTYX) is up 56% after the Wall Street Journal reported that Eli Lilly & Co. is in advanced talks to acquire the company for more than $1 billion to expand its work in immunology.

In corporate news, MSCI decided against excluding digital-asset treasury companies from its MSCI Global Investable Market Indexes in its February review, sending Strategy higher in extended trading. And an Amazon AI tool offered merchants’ products without their consent.

Stocks have been on a tear on optimism over solid earnings growth and inflation remaining sufficiently contained for the Federal Reserve to keep cutting interest rates. That optimism has persisted despite a worsening geopolitical backdrop, including US actions in Venezuela, its threats of intervention elsewhere and rising tensions between China and Japan. But on Wednesday, the global rally stalled with geopolitical strains dampening the mood. Three big days of data are kicking off, with JOLTS job openings and ADP numbers due later. Memory chip shortages are in focus for AI bulls.

“Shifting trends create uncertainties that need to be priced into assets,” said Florian Ielpo, head of macro and multi-asset at Lombard Odier. “We are talking about a breathing period, with investors taking time to rethink how to deploy their concentrated equity investments in a deconcentrating world.”

Mining stocks were among the biggest decliners in premarket trading, with Newmont Corp., Freeport-McMoRan Inc. and Barrick Mining Corp. all down 1% or more. Precious metals joined the broader pullback, with silver falling below $80 an ounce and gold breaking a three-day winning streak. Copper retreated from an all-time high.

For AI bulls, memory chips are in focus after comments from Nvidia’s Jensen Huang about the need for memory and storage at CES on Tuesday. Stocks including Sandisk and Western Digital have surged in the past few days, and the rally is likely to continue: Samsung expects shortages to drive price hikes and DRAM specialist Nanya posted 445% year-on-year sales growth for December.

Three key days of economic data kick off on Wednesday as investors track the Fed’s likely path for rates, with November jobs openings and ADP Research’s private-sector payrolls figures due. The Institute for Supply Management’s index of services is expected to show a slight moderation in December activity.

“Further declines in the JOLTS hiring and quit rates would add to signs of worsening labor demand,” wrote Elias Haddad, global head of markets strategy at Brown Brothers Harriman. “If so, it would validate the 50 basis points of cuts priced into Fed funds futures over 2026 and weigh on the dollar.”

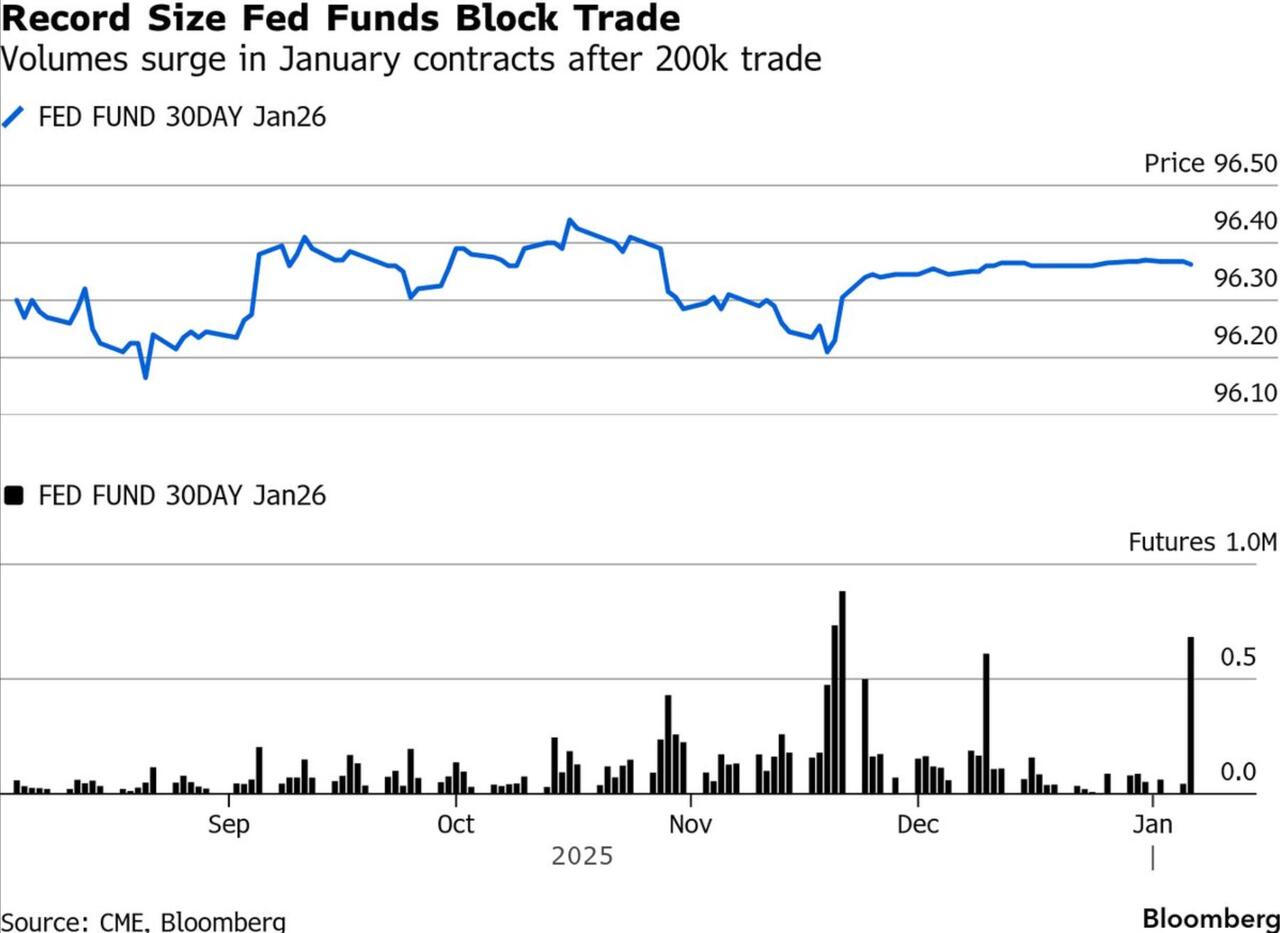

Ahead of a slate of data in the next few days, a record-sized block trade was placed in the federal funds futures market. The trade was struck in the January contracts for a size of 200,000, the largest ever as confirmed by CME Group. The motive behind the transaction is unclear. It could be related to an unwinding of existing bets or a wager that could benefit from a potential shift in market pricing for the Fed’s next rate decision.

Other developments rattling sentiment include comments from the White House that Trump is considering many ways of acquiring Greenland, and won’t rule out the use of military force. In Asia, China escalated a feud with Japan by announcing a probe on chipmaking material, while rare earth stocks surged on the back of new China-Japan export curbs.

In Europe, the Stoxx 600 is little changed with energy stocks a drag as oil prices slide. Energy stocks lag after President Donald Trump said Venezuela would send oil worth up to $2.8 billion to the US, while utilities outperform.

Here are some of the biggest movers on Wednesday:

- Italgas shares rise as much as 10% to hit a new record high after gas distribution operator Snam announced an offer of green bonds due 2031 in an aggregate notional amount of €500m, exchangeable for existing ordinary shares of Italgas.

- Thyssenkrupp shares gain as much as 5.3%, leading defense stocks higher after the Trump administration and Ukraine’s allies moved toward an agreement to offer security guarantees long sought by Kyiv.

- ArcelorMittal shares climb as much as 3.5% to the highest level in nearly 14 years after Morgan Stanley installed the stock as top pick in Europe’s steel sector.

- Atlas Copco shares rise as much as 9% to the highest level since February after Bernstein upgrades on expectations that earnings have bottomed.

- InPost shares retreat as much as 8.3%, ceding some of the previous day’s 28% gain triggered by the parcel locker operator’s announcement of a takeover proposal.

- Fresnillo shares drop as much as 4.1%, leading precious metal miners lower as gold prices decline.

- NatWest shares fall as much as 3% after they are downgraded to equal-weight from overweight at Barclays.

- Equinor shares slip as much as 3.8% as European oil stocks track crude prices downwards after Trump said Venezuela would relinquish as much as 50 million barrels of oil to the US.

- Kingspan shares drop as much as 5.4% after the company said it won’t pursue an IPO of Advnsys and will continue to report the data center materials unit as a wholly owned and broadly distinct reporting segment.

- Redcare Pharmacy shares plunge as much as 9.7%, the most since August, after the company posted fourth-quarter sales that came in below expectations due to weakness in over-the-counter products.

Earlier in the session, Asian equities declined, as escalating trade tensions between China and Japan damped investor sentiment following the recent rally. The MSCI Asia Pacific Index dropped as much as 0.7%, poised to snap a four-day advance. Technology megacaps including TSMC and Tencent were among the biggest drags, while Alibaba dropped on fresh concerns over Beijing regulations. A key gauge of Chinese stocks listed in Hong Kong led losses, while benchmarks in Japan and Taiwan also fell. China imposed controls on exports to Japan with potential military uses, intensifying a standoff between Asia’s top economies in a dispute related to Taiwan. Automakers were the biggest contributor to losses in Japan on the news. The Japan-China squabble is causing some jitters after a strong start to the year for the region’s stocks. The rally had also started to show signs of overheating. The 14-day relative strength index for the MSCI Asia Pacific Index climbed above 70 this week, entering technical overbought territory for the first time since early October.

In rates, treasury futures hold gains accumulated during London morning amid bigger rallies in European bond markets spurred in part by weak German retail sales data for November. US yields richer by 1bp-4bp across a flatter yield curve, with 2s10s and 5s30s spreads respectively 3bp and 2bp tighter; 10-year near 4.145% is about 3bp richer by 3bp on the day with bunds and gilts in the sector outperforming by 1.5bp and 4.5bp. European government bonds advance for a third day, with buying more pronounced at the longer end of the curve. German 10-year yields fall 4 bps to a one-month low after weak economic data prompted traders to increase their bets on interest-rate cuts by the European Central Bank. Gilts outperform, with UK 10-year borrowing costs sliding 7 bps. European borrowers brought a record number of tranches to the market on Wednesday and are set to raise at least €38.1 billion ($44.5 billion), a number that’s likely to increase over the course of the day. Issuance in the US investment-grade bond market topped $72 billion in the first two days of the week, according to data compiled by Bloomberg. Focal points of US session include December ADP employment change and ISM services gauge and November JOLTs job openings.

In commodities, WTI crude futures fall 0.5% to $56.80 a barrel after Washington moved to exert greater control over Venezuela’s industry, with President Donald Trump saying the country would turn over millions of barrels to the US. West Texas Intermediate traded near $57 a barrel. Investors were also keeping tabs on the primary bond market as the first week of 2026 saw a surge in global issuance, signaling strong confidence despite heightened geopolitical risks. Spot silver falls 2% and back below $80/oz. Gold also drops. Bitcoin is down 1.3% near $92,000.

Today's US economic calendar includes December ADP employment change (8:15am), December ISM services index, November JOLTS job openings and October factors orders (10am). Scheduled Fed speakers include Bowman on banking supervision and regulation at 4:10pm. Albertsons is scheduled to report results before the market open. Earnings from Jefferies and Costco December sales are due later in the day.

Market Snapshot

- S&P 500 mini -0.2%

- Nasdaq 100 mini -0.3%

- Russell 2000 mini little changed

- Stoxx Europe 600 little changed, DAX +0.6%

- CAC 40 -0.2%

- 10-year Treasury yield -3 basis points at 4.14%

- VIX +0.4 points at 15.15

- Bloomberg Dollar Index little changed at 1205.69

- euro little changed at $1.1692

- WTI crude -0.9% at $56.59/barrel

Top Overnight News

- Marco Rubio has told lawmakers that President Trump plans to buy Greenland rather than invade it, while Trump has asked aids to give him an updated plan for acquiring the territory. NYT

- Trump will meet with oil company chief executives Friday at the White House to discuss plans for them to enter Venezuela and drill. Trump announced that Venezuela would relinquish 30 to 50 million barrels of oil to the US, worth roughly $2.8 billion at the current market price. BBG

- China's Foreign Ministry said China's legitimate rights and interest in Venezuela must be protected, in regards to US President Trump's statement on Venezuela oil.

- The US for the first time on Tuesday backed a broad coalition of Ukraine's allies in vowing to provide security guarantees that leaders said would include binding commitments to support the country if Russia attacks again. RTRS

- Chevron and private equity firm Quantum Capital Group are teaming up on a bid to buy the international assets of sanctioned Russian oil company Lukoil. FT

- China launched an anti-dumping probe into Japan’s chipmaking material dichlorosilane, deepening trade tensions after Beijing imposed export curbs — potentially affecting over 40% of its shipments to the country. Tokyo called the measures unacceptable. BBG

- AI “fatigue” is driving cash into shares of S&P 500 companies that aren’t the Magnificent 7, especially those that would benefit most if an expected uptick in economic growth materializes. BBG

- old is neck and neck with Treasuries to become the biggest reserve asset for foreign governments, driven by a year of explosive price gains and aggressive central bank buying. Barron’s

- Eurozone CPI for Dec was inline on the headline at +2% (down from +2.1% in Nov) while core cooled to +2.3% (vs. the Street +2.4% and down from +2.4% in Nov). BBG

- Waner Bros. Discovery Board of Directors unanimously recommended shareholders reject amended Paramount tender offer, saying the offer remains ‘Inadequate.’ BBG

- Goldman forecast MSCI China and CSI300 to appreciate 20% and 12% in 2026, after key benchmarks gained 20%-30% in the past year mainly on multiple expansion.

Trade/Tariffs

- China's Commerce Ministry announces an anti-dumping probe into Japan Dichlorosilane imports; investigation begins on Jan 7 and will end a year later, but can be extended by 6 months if needed.

- Japanese Chief Cabinet Secretary Kihara said China curbs targeting only Japan are regrettable, adds we'll consider necessary response as we assess China's export curb details.

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded somewhat mixed as momentum began to wane despite the fresh record levels on Wall Street. ASX 200 marginally gained amid strength in tech and defensives, while participants also digested monthly inflation data, which printed softer-than-expected but remained sticky. Nikkei 225 lagged amid Japan's frictions with China after the latter imposed export controls on dual-use items to Japan. Hang Seng and Shanghai Comp retreated with the Hong Kong benchmark pressured by losses in energy names and tech stocks following a decline in oil prices, and with platform names pressured by China announcing management measures for online platforms. Meanwhile, the mainland bourses kept afloat for most of the session but eventually faltered as the mood deteriorated and were also not helped by a substantial net liquidity drain of around CNY 500bln in the PBoC's open market operations.

Top Asian News

- Maersk (MAERSKB DC) said Asia-Pacific ocean freight markets enter 2026 with cautious optimism; intra-Asia volumes are gaining momentum, and supply chain planning is increasingly focused on agility, regional connectivity, and early Chinese NY preparations.

- South Korea's President Lee said had a serious talk with China regarding supply chains and peace on the Korean Peninsula.

- Baidu's (9888 HK) AI chip arm Kunlunxin aims to raise up to USD 2bln in Hong Kong IPO, according to Bloomberg citing sources. – Co. has picked China International Capital Corp., Citic Securities Co. and Huatai Securities, while China Securities International is also working on the potential offering.

- UMC (2303 TT) Dec (TWD): Revenue 19.3bln (prev. 19.0bln Y/Y).

- China's market regulator and cyberspace authorities unveiled two separate documents on Wednesday to further regulate the country's livestreaming e-commerce sector and online trading platforms, Xinhua reported.

- China announces management measures for online platforms and China's market regulator said online platforms must not sell below cost or disrupt market competition. Online platforms must not sell below cost or disrupt market competition.

European bourses are mixed. The FTSE 100 (-0.6%) is under pressure, hit by losses across underlying commodity prices whilst the DAX 40 (+0.6%) posts gains by around half a percent. European sectors hold a very slight negative bias. Utilities holds towards the top of the pile, joined closely by Construction & Materials, and Real Estate. To the downside, Energy is the laggard, in-fitting with pressure seen across crude benchmarks whilst Luxury downside weighs on Consumer Products & Services.

Top European News

- Italian PM Meloni plans overhaul of Italy's voting system to aid re-election bid, according to FT.

FX

- DXY is flat intraday but resides in a current 98.497-98.690 parameter as traders await key US labour market data due ahead of Friday's official employment situation report; ADP's gauge of nonfarm employment is expected to print 49K in December vs -32K in November. JOLTS job openings are expected to fall to 7.61mln in November (prev. 7.67mln in October); in the October report, the quits rate fell to 1.8% from 2.0%, while the vacancy rate was unchanged at 4.6%. Elsewhere, the ISM Services PMI is seen inching down a little in December. Currently, the index is well within Monday’s 98.25-98.86 range, and on either side of its 100 DMA (98.59).

- EUR/USD was initially pressured, continuing the downside seen in the prior session. Though the downside did reverse following the EZ HICP release, which printed in-line with expectations, seemingly as bets for a cooler-than-expected print following the German series unwind. Currently just shy of the 1.1700 mark, after making a peak of 1.1702 overnight.

- AUD/USD is choppy following overnight outperformance given softer-than-expected monthly inflation, but as the headline figure and the core reading remain sticky and above the RBA’s 2-3% target.

- USD/JPY found resistance at yesterday’s high and remains