Production For Security 2026

Submitted by Peter Tchir of Academy Securities

ProSec 2026

We will do a “traditional” outlook for 2026, covering all major markets, but we really wanted to highlight ProSec and define more carefully what we think it means for you as corporations, policy makers, and asset managers.

Production for Security:

-

RESILIENCY. We haven’t used the word “resiliency” as much as we could have and will use it more going forward. Being resilient, whether at the nation, state, or corporate level, will become a fixture in decision making.

-

ProSec is already in the process of supplanting “traditional” ESG as an overarching theme in decision-making and planning.

-

As much as we’ve tried to instill our view on how big, broad, and important the scope of ProSec is, we have failed to do that – so far.

-

While not critical to ProSec we do believe that as the world adopts a “Pre-War” mentality, it helps accelerate ProSec as it imbues a degree of “sacrifice for the greater good” while also imparting a sense of “urgency.”

-

ProSec is already going global and getting left behind on this initiative will be problematic for countries, companies, and investors.

Resiliency as a Driving Force Behind ProSec

To some degree we can describe ProSec as being the answer to “What If?”

-

What if global shipping is disrupted?

-

It has happened for reasons “out of our control.” COVID was not on anyone’s radar screen. Even the Evergreen blocking the Suez Canal was an “unforeseen” accident. Will markets react the same the next time around to companies exposed to that risk? What if some companies have “planned” for this and have more robust supply chains – less use of shipping, using a variety of shipping lanes, only shipping with countries they are very close to – physically or politically? If a “competitor” has prepared and you haven’t, and it occurs again, it is difficult to see markets being as “understanding” as they were when it was deemed farfetched.

-

Legend has it that the disaster recovery plan for one incredibly large hedge fund was to use other offices as disaster recovery sites. It had the advantage of being global, so if something happened in a region that took out the main office, and the disaster recovery site, it would still be covered. It had the advantage of all sites being up to date. Nothing worse than getting to the disaster recovery site and realizing that the internet is too slow and you were running obsolete versions of software. The plan made a lot of sense. It did not cover the contingency of grounding all U.S. flights for days. To the extent the story is true (and I have no reason to doubt it), I can assure you that this fund revamped their plans to cover even more contingencies as well as other highly unlikely, but still possible scenarios. They increased their RESILIENCY as they absorbed new information.

-

-

-

It happened because a “bad actor” behaved badly. Prior to the invasion of Ukraine by Russia, we could explain being “asleep at the switch” in terms of this type of risk. Iran and its proxies attacking more aggressively in the Middle East has not caused major disruptions, but it has caused some level of disruption, and seemed like a more foreseeable event than Russia’s invasion. The U.S. has just “blockaded” Venezuela. Actually, we did not “blockade” Venezuela as that is an act of war according to international law, but we have changed the nature of doing business with Venezuela.

-

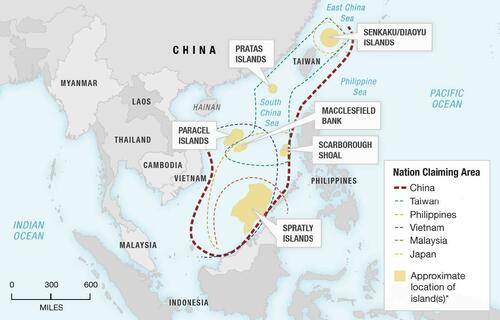

The People’s Armed Forces Maritime Militia (PAFMM). We used GROK for some of this information, but it is all very consistent with topics we’ve discussed in the past. Let’s start with this map from GROK attributed to npr.org to explain some potential risks.

It (PAFMM) often operates in coordination with the PLA Navy (PLAN) and China’s Coast Guard (CCG) as part of a "joint defense" approach involving military, law enforcement, and civilian elements. In peacetime, it contributes to gray-zone tactics—coercive actions short of open warfare—such as swarming disputed features, harassing foreign vessels, or establishing a de facto presence to bolster territorial claims in the South China Sea and East China Sea. Western analyses describe it as enabling China to advance its interests while maintaining plausible deniability, as vessels appear to be civilian. Chinese sources emphasize its role in leading fishing activities, collecting oceanic information, supporting island/reef construction, and participating in drills for national defense and disaster relief.They have had as many as 400 ships active at any one time. According to GROK the “professional” component consists of 100-200 purpose-built boats (presumably larger and more sophisticated ones). There have been estimates that the total number of ships available is in the thousands. While not set up to attack, in the traditional sense, they can make sea travel perilous, not only by getting in the way, but also by dumping things like nets and logs overboard to foul propellors, etc.

The main focus today is Taiwan, because of our dependance on Taiwan for chips (a recurring theme of our 2026 Outlook), but it seems almost naïve to believe that there isn’t a bigger risk to shipping than just the concern around Taiwan’s chips (which in and of itself is a risk unless we become more “resilient” or diverse in our chip businesses).

We didn’t even touch on China’s control, ownership, and equipment in many ports across the globe as a potential future risk, but it certainly is.

-

- While we might not lose sleep every night worrying about shipping lanes, it seems prudent to plan for the worst if the cost to diversifying shipping lanes is small.

Considering the latest National Security Strategy, the potential safety of shipping should be a consideration when building new facilities. That gives the nod to North, South, and Central America, especially if you are not already overly exposed to the region.

- What if the flow of processed or refined rare earths and critical minerals is cut off?

- Clearly this would be a risk if shipping with China is disrupted. But given what we’ve seen with the trade negotiations, it seems easy to play out scenarios where China decides to curtail shipments of their own volition.

These scenarios are by no means the base case, but do you really believe they have a zero probability of occurring? That there is no set of circumstances in the next few years under which China decides it is in their best interest to reduce shipments of these materials? Antimony is used in every munition and we remain highly dependent on China for this.

I am more focused on the refined and processed versions. China controls about 60% of the extraction/mining of what is broadly categorized as rare earths and critical minerals. They control about 90% of the processing and refining.

They can shut us off from the raw resources, but we could, in most cases, source them elsewhere. However, what good does it do if we have to ship them to China to be refined and processed?

I know I don’t always do a good job of highlighting the importance of these “things.” It is almost easy to dismiss some as they are “only a small part” of a bigger item. When we think “big picture,” it is easy to forget the importance that these little parts play in the grand scheme of things. Often, they are not just a little portion, but a large portion – when you are talking about batteries for instance.

With the help of OpenAI I have tried to bring the CEO of Whirlpool’s comments (made during COVID) to life.

This is maybe too “casual” or even too “obvious” as of course a washing machine needs a door, but that doesn’t make the point irrelevant (just my choice of graphics).

So much of our industrial production could grind to a halt, just because some small amount of processed/refined rare earths or critical minerals (that we depend on China for) doesn’t make it to our factories. It doesn’t only have to be to our “domestic” factories; this applies to factories anywhere around the globe, maybe even within China, if they decide to go down this path.

Again, it isn’t our base case, but becoming more RESILIENT, aka ProSec, goes a long way towards mitigating this risk.

While we don’t need to be completely “self-sufficient,” the more we can produce on our own, the more likely China won’t try to cut us off.

- Clearly this would be a risk if shipping with China is disrupted. But given what we’ve seen with the trade negotiations, it seems easy to play out scenarios where China decides to curtail shipments of their own volition.

-

Energy and electricity production.

-

Germany and Russian Natural Gas. Enough said.

-

We need to think about resiliency. We need realistic and cost effective contingency plans. The “irony” of this is the more independent one becomes, the less chance one becomes the target of an adversary or competitor. It is effectively Economic Deterrence.

Maslow’s Hierarchy of Economic Needs

Of all the things I learned in college, being able to open a bottle of beer with another beer and Maslow’s Hierarchy of Needs might be the two most useful things I learned (though to be honest, growing up in Canada, I think we learned the beer bottle thing in high school, but I digress).

I don’t know what “self-actualization” really is, but Universal Basic Income seems right up there. I previously thought we were in the “Esteem” stage. That let us think about things differently. The concern I have is that we were being overly “altruistic” in our vision because we thought we had the levels below us covered. The crumbling foundation is what has become apparent, first gradually, and then suddenly.

We have published on many of these themes going back to 2018. They aren’t completely new.

COVID did change a little of how we think and behave, especially towards China.

The Biden administration saw the need for the CHIPS ACT.

But all of these things seemed more like an attempt to patch a crack, rather than determining that the entire foundation might be crumbling and needs to be completely redone!

ProSec and ESG are Compatible

Despite how the previous section might come across, much of what “we” were trying to achieve with ESG will remain in place. But the lens through which we look at ESG will be changing with “true” Sustainability (Resiliency, Independence, Security, etc.) taking center stage.

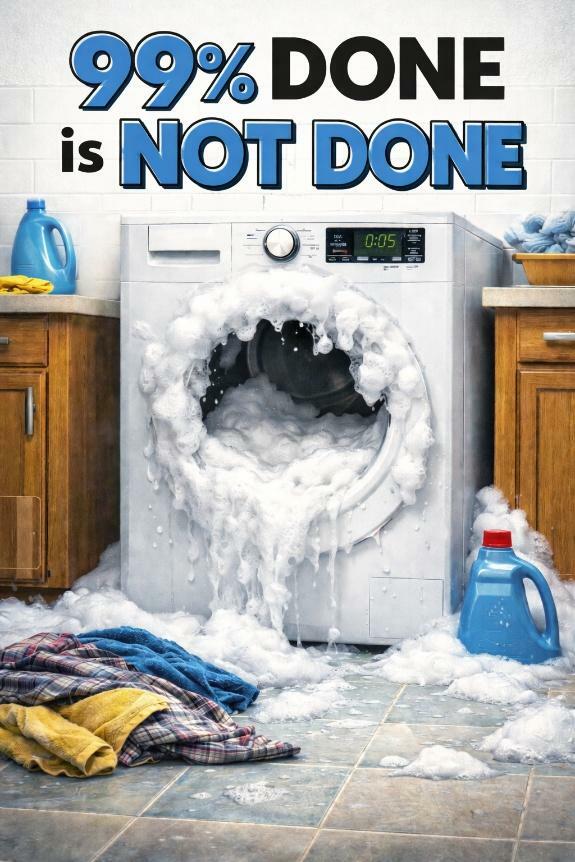

The ProSec Industries.

Let’s take a “quick” look at how we see the ProSec economy developing around specific industries.

This chart is intended to do a few things:

-

Make you wish that I’d figured out how to use AI to make this chart more professional.

-

Highlight the industries with some sense of relative importance (column width).

-

Highlight how much can be done easily (green), with some effort (yellow), facing some real hurdles (orange), and some that might not be achievable (red).

Biotech and Pharma.

-

As a “talking point,” reducing healthcare costs is easy. The complexity of the system makes it difficult. Same for “manufacturing at home.” On the surface it is “easy,” but there are a lot of difficulties. Hundreds, and even thousands of drugs are produced. We can kind of get away with saying “steel” and it covers the topic reasonably well (though purists would argue about the type of steel, etc.). But “drugs” is just too vague. There are the components, the base, and precursor drugs. There are the complex drugs we actually ingest or take. There are drugs with multiple delivery methods. The delivery methods themselves are sometimes separated from the drug itself. Patents. There is a focus here, but it is so complex that I think only slow progress will be made.

-

For the “green” section of this industry, look no further than the GLP-1 drugs. They have the benefit of being topical and potentially have incredibly widespread application. Certainly, interest in them is widespread. The combination of “big and public” makes them an ideal candidate for an administration to focus on. Lots of headlines and manageable. Away from that, it seems like it will be a slog to get a lot of manufacturing done here. It will happen over time (we had immense success getting the COVID vaccines produced here – regardless of your view on the vaccines themselves).

-

My best guess is that the admin will focus on the pharmacies next, rather than the manufacturers, as that industry is concentrated, and well known to the public, so easier to get a lot of “bang for the buck” on the political front. While I think this is an incredibly important ProSec industry, I think it will not be front and center in 2026 for opportunities.

Chips, Data Centers, and AI.

-

These industries are doing incredibly well in their own right. Demand is there. In terms of ProSec™ the goal of the administration will be to bring more and more production home. There are a lot of opportunities in this space. The industry leaders should continue to do well and get government support. That support might come in many forms. Some of it may be through increased government use of the services. The government (in all facets, including state, local, defense, and healthcare) will spend in this sector.

-

Regulatory help is another avenue the government will pursue. Whether paving the way for data centers, the power generation required, or even allowing products to be exported, to earn money, and to fund domestic growth, there will be support from the administration.

-

INTC continues to stand out in this sector. While I would like rules in place to regulate state investments, those are not really in place (and would likely be pushed to the limit by this admin, even if they were in place). I find it difficult to see a world where the government doesn’t try to support the taxpayers’ investment in this company. For full disclosure, INTC was my biggest single stock holding in 2025 and will be again in 2026. It was up 86% in 2025. Can it repeat that? Who knows, but while I think any stock in this space has potential, with those focused on manufacturing in the U.S. getting the most government support, the direct investment leads me to suspect that extra support will be given here.

-

Much of this chart is “green” and even “yellow” as a lot remains in our control. Look for a “shift” in the industry as it moves to where the energy (electricity) and fresh water are located. Tasks that require low latency will remain in locations that can offer that speed, but applications that allow for more latency will move to where the electricity is.

-

The administration is likely going to take a closer look at quantum computing. I briefly pulled up WQTM (a quantum ETF) and some of their holdings jumped out at me – QBTS, IONQ, RGTI, and ARQQ to name a few. I have not spent much time on this, but some of these stocks seem to fit the “lottery ticket” theme in ProSec™ (companies with a small enough market cap, that a direct investment by the U.S. taxpayers could help the stock “pop,” similar to the investment in MP – though that stock is well off of its highs).

Electron Production.

-

There will be a focus on not only producing the electricity needed for AI, Data Centers, EVs, and industry, but also getting it to where it needs to go (transmission).

-

All forms of electricity generation will be used. Okay, maybe all forms other than wind, which this administration seems to really dislike.

-

Fusion. This is more the “future” and I haven’t poked around for tickers, but makes sense.

-

Fission. This is an area we have focused on a lot. The government is clearly promoting the growth of the nuclear power business. From allowing nuclear to be built on Army bases, to chatter about using Navy reactors more broadly, the government is working hard to jumpstart the nuclear industry. It has the longest lead time to build. There remains a “fear” factor associated with nuclear (I wonder what the world would look like had the nuclear industry hired the Bitcoin marketing team ). Despite those risks (too long and too much negative public opinion) I think the opportunities remain very good in this space.

-

URA is an ETF that focuses on Uranium. One way to bet on the rise of nuclear, here and abroad (Canada for example is ramping up efforts in this area), is through Uranium. The commodity itself, the miners, and the refiners could all do well if the nuclear industry really takes off. Worth looking through the holding of ETFs like this to assess what stocks might make sense.

-

Personally, I’m fascinated with the Small Nuclear Reactor space. It has been a roller coaster ride, and we need to see projects completed, in scale, but this fits our theme extremely well.

-

-

Coal and Natural Gas. While nuclear might become the backbone years from now, we are going to need rapid expansion of coal and natural gas burning facilities. Ma

-