Global Stock Rally Fizzles, Futures Flat As Market Rotations Accelerate

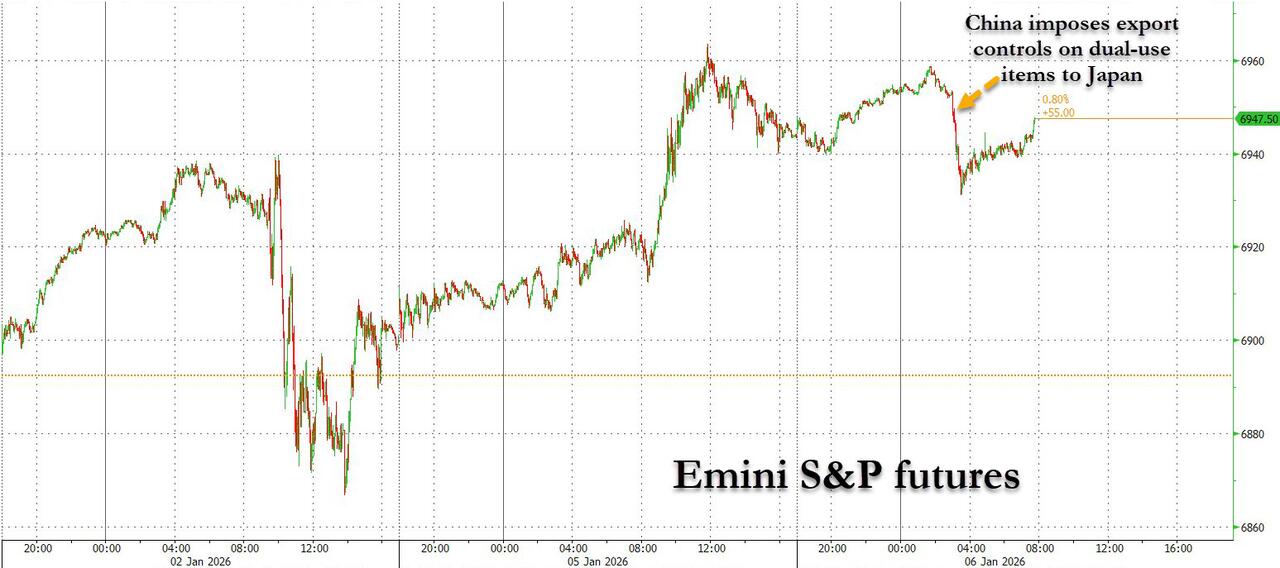

US equity futures are flat with small caps underperforming as geopolitics dominate headlines, including aftershocks from the Maduro seizure and a potential US/EU deal that provides a security guarantee for Ukraine potentially with American soldiers maintaining a presence in Ukraine. As of 8:00am ET, S&P futures are flat as a rotation into regional shares broadened and investors awaited fresh data to gauge the outlook for Federal Reserve interest rates; Nasdaq futures gain 0.2% even as Mag 7 names are weaker premarket ex-NVDA which is leading Semis higher after Jensen Huang's CES presentation. Futures took a brief spill overnight just around 3am ET when China announced it would launch export controls on Japan, which is negative for heavy machinery; futures then promptly recovered. Defensives are leading Cyclicals ex-Energy. Bond yields are higher by 1-2bp with USD also bid. Major European markets are mixed with UK leading and France lagging. Asian stocks are off to their best start since 2012 with the MXAP up 3% YTD. Today's US economic calendar includes December final S&P Global US services and composite PMIs at 9:45am. Scheduled Fed speakers include Barkin (8am) and Miran (8:30am)

In premarket trading Mag 7 names are mixed, with Nvidia gaining 0.6% as CEO Jensen Huang said the company’s much-anticipated Rubin data center processors are in production and customers will soon be able to try out the technology.(Alphabet +0.2%, Microsoft is flat, Amazon -0.08%, Meta +0.9%, Apple -0.3%, Tesla -0.6%).

- Aeva (AEVA) jumps 23% after the company announced that its 4D LiDAR technology has been selected for the Nvidia Drive Hyperion autonomous vehicle reference platform.

- Core Scientific (CORZ) climbs 4% as BTIG upgrades to buy as the dust settles following shareholder rejection in October of its acquisition by CoreWeave.

- Frontier Group (ULCC) falls 3% after BofA cut the recommendation on the airline to underperform, expecting cost challenges in 2026 as aircraft rental fees rise.

- Microchip (MCHP) rises 4% after the analog chipmaker’s net sales forecast for the third quarter beat the average analyst estimate. Analysts note that the strong sales numbers highlight broad-based recovery.

- Oculis (OCS) rises 8% after the drug developer said its experimental therapy, Privosegtor, was granted the FDA’s breakthrough therapy designation for the treatment of optic neuritis — inflammation of the eye nerve.

- OneStream Inc. (OS) soars 22% as buyout firm Hg is in advanced talks to acquire the financial software maker, according to people familiar with the matter.

- Vistra Corp. (VST) climbs 4% after agreeing to pay roughly $4 billion for 10 natural gas-fired power plants in the US Northeast and Texas to expand the electricity supplier’s generation capacity in fast-growing energy markets.

- Zeta Global (ZETA) rises 9% after the software company announced that it has entered a strategic collaboration with OpenAI to power conversational intelligence and agentic applications behind Athena by Zeta, its superintelligent agent built for enterprise marketing.

In other corporate news, AB InBev will reacquire a 49.9% stake in US metal plants from a consortium of investors for $3 billion. Electricity supplier Vistra agreed to pay roughly $4 billion for 10 natural gas-fired power plants in the US Northeast and Texas. Software company Zeta Global announced a strategic collaboration with OpenAI.

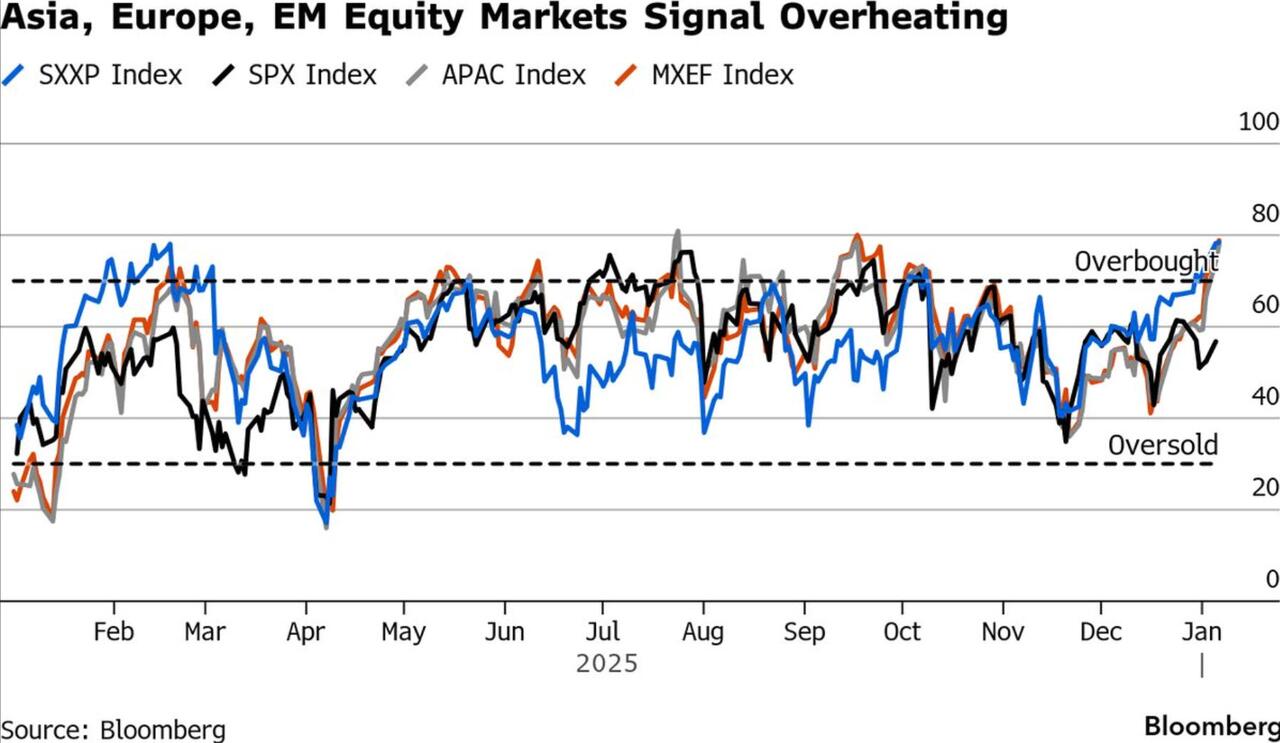

The New Year rally appears to be losing steam, despite renewed appetite for the AI trade and cyclicals over defensives. Some of the biggest action is in commodities, with an index of base metals surging to the highest since March 2022 and copper rising above $13,000 a ton for the first time, which needless to say, is and will be inflationary. At the same time, stocks in Asia surged, but as Bloomberg notes, are now getting dangerously overbought, along with markets in Europe and emerging markets. The S&P 500’s 14-day relative strength index also suggests that US stocks might have further room to run, in contrast with other regions that have surpassed levels typically seen as overbought. Macro and geopolitical risks are numerous, with Venezuela, Greenland and Taiwan all in the headlines today.

Stock investors have so far been largely unfazed by tensions in Venezuela, extending a three-year bull run that’s been fueled by demand for AI–linked shares. The next leg of the rally will depend in part on how quickly the Fed moves to further ease monetary policy, with business activity and jobs market data due this week to help shape rate expectations.

“We are waiting for data,” said Emilie Tetard, a cross-asset strategist at Natixis. “Before this data, as macro uncertainty is probably stronger in the US vs. the rest of the world, it’s a good time to put in place the diversification.”

Meanwhile, US oil producers such as Chevron Corp. and ConocoPhillips extended gains on President Donald Trump’s plans for the reconstruction of Venezuela’s crude industry.

The AI narrative is getting a boost from announcements at CES. AMD unveiled a new chip for corporate data centers, with CEO Lisa Su noting on AI that “we don’t have nearly enough compute for what we could possibly do.” Nvidia CEO Jensen Huang said the company’s highly-anticipated Rubin processors are on track for deployment by customers in the second half. “Demand is really high,” he said. And Intel’s comeback bid is relying on laptops shown at CES that are based on processors with a new design. As Bear Traps report Larry McDonald puts it, "the Pumpmaster is on Stage Again": Nvidia CEO Huang keynote address confirmed that Vera Rubin is now in full production and is expected to propel Nvidia back into the position of undisputed technical leader. Jensen noted that Vera Rubin contains 6 separate, revolutionary chips, and in years past, each one would have been made by a separate company, but Nvidia does them all itself.

In the geopolitical sphere, Venezuela’s new acting president Delcy Rodríguez is seen as a choice that could stabilize Venezuela’s oil-based economy and facilitate American business. Elsewhere, Trump’s rationale for intervening in Venezuela is fueling concerns among European officials that they could soon face an existential dilemma over Greenland.

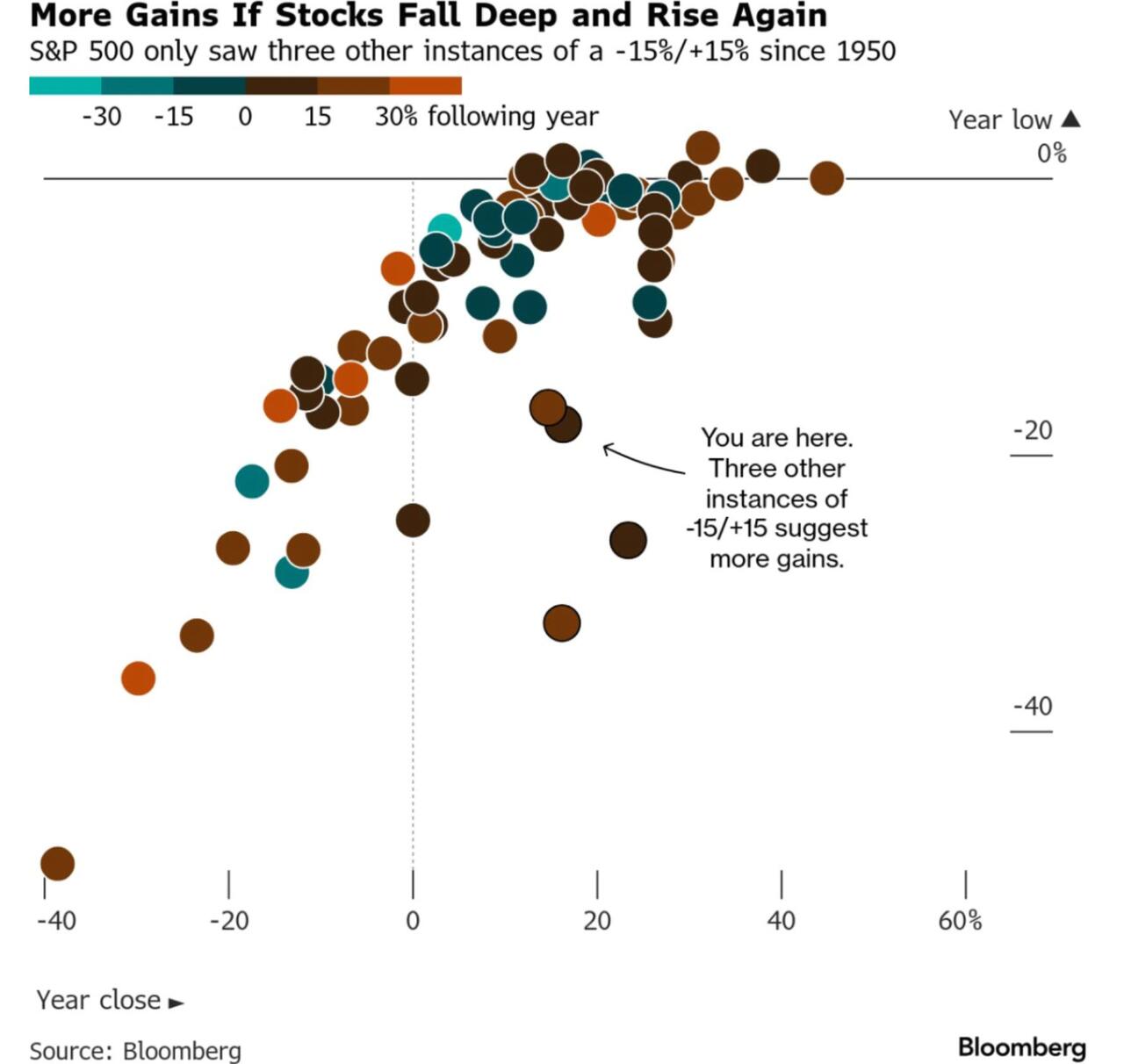

Elsewhere, the data may be on the side of bulls. According to Bloomberg, there have been just four years when the S&P 500 fell at least 15% and and still managed to achieve an annual advance of 15% or more. It happened in 1982, 2009, 2020 — and in 2025. The previous cases have all been followed by strong gains during the next year. Still, Wall Street bulls need a lot to go right if 2026 is going to deliver a fourth straight year of double-digit returns. Read more in today’s Taking Stock.

European stocks are mixed regionally, with the broad Stoxx 600 higher by 0.2%; health care leads, tech lags while miners are lifted after copper surged to a fresh record amid a renewed rush to ship the base metal to the US. Consumer products and services shares lag, with Adidas tailing the sector. Here are some of the biggest movers on Tuesday:

- InPost shares rise as much as 20% after the Polish logistics firm announced it had received an indicative proposal regarding a potential acquisition.

- Next shares climb as much as 3.7%, the most since October, after the fashion retailer reported strong Christmas sales and boosted its profit guidance for the fifth time this financial year.

- Tesco shares climb as much as 3.4% after Worldpanel by Numerator said the British grocer had increased sales and market share in the run-up to Christmas, taking its greatest slice of shoppers’ spend in more than a decade.

- Daimler Truck shares rise as much as 5.6%, hitting the highest level in four months, after the release of positive data for a key measure of North American truck orders.

- SMG Swiss Marketplace Group shares surge as much as a record 17%, after it announced an “amicable” agreement with Switzerland’s Price Supervisor regarding investigations into the Ricardo platform and SMG Real Estate business.

- Infineon shares rise as much as 5.1% after US peer Microchip gave an upbeat forecast and Bank of America lifted its price target, partly due to AI server exposure.

- Adidas shares fall as much as 7.6% after Bank of America downgraded the stock to underperform, predicting a “material stepdown” in growth for the sportswear sector. Retailer JD Sports was cut to neutral, and its shares fall 7.2%.

- DSM-Firmenich shares drop as much as 1.3% after Morgan Stanley downgraded the stock to equal-weight, citing lingering uncertainty around the animal, nutrition and health exit structure and tough mid-term strategic targets for the core business.

- Liontrust Asset Management shares sink as much as 7.7%, the most in six months, as Deutsche Bank analysts cut their recommendation on the firm to sell from hold, and slash the target price by a third.

“It reflects a continuation of a theme that we are in the early innings of, which started last year, i.e. that US exceptionalism has peaked and has started to unwind,” Raymond Sagayam, managing partner at Banque Pictet & Cie SA, told Bloomberg TV.

Asian equities rose to a fresh record high, with a rally in Chinese shares helping fuel stronger risk appetite for the region. The MSCI Asia Pacific Index advanced 1.2%, poised for a fourth straight day of gains in what is poised to be its best-ever start to a year. Tech again remained a focus, with TSMC, SK Hynix and Hitachi among the biggest contributors to the benchmark’s advance. Key gauges in mainland China, Hong Kong as well as Japan rose more than 1%. China’s onshore CSI 300 Index climbed to the highest in four years on enthusiasm for the country’s AI industry and growing signs of an economic recovery. Investors hope for an extension of last year’s gains as Beijing backs key sectors and implements measures to curb excessive competition and revive the ailing property market. A subindex of financial shares also helped boost the Asian benchmark, after US peers climbed overnight. Japanese banks jumped after central bank Governor Ueda said he intends to keep raising rates in line with inflation. The rally in Asian stocks at the start of the year underscores their rising appeal for global investors wary of high tech valuations in the US and the prospect of a weakening dollar. It also points to the room left to run in the region’s tech shares, with Samsung Electronics Co. and Taiwan Semiconductor Manufacturing Co. powering the gains over the past few days.

In FX, German inflation weighed on the euro, lifting the Bloomberg Dollar Index higher by 0.1%. G-10 FX moves are limited.

In rates, treasuries hold small losses in early US session, unwinding a portion of Monday’s gains with oil futures rising further and stock index futures stalled near record highs. European bonds outperform following soft German regional inflation prints. US yields are 1bp-2bp cheaper with curve spreads steeper; 2s10s topped 72bp, approaching 2025 wides; 10-year near 4.17% is about 1bp cheaper on the day, with bunds and gilts in the sector outperforming by about 3bp. German yields are lower by around 2bps across the curve following soft regional inflation metrics. In contrast, US yields are higher with the curve bear-steepening.

In commodities, WTI crude futures are building on yesterday’s gains, up 0.3%. There’s mixed fortunes for precious metals with spot silver higher by 2.2%. Gold faded initial gains and is now up just 0.2% while LME copper hit further all-time-highs, up 1.3%.Bitcoin has slipped throughout the session, trades lower by 0.4%.

US economic calendar includes December final S&P Global US services and composite PMIs at 9:45am. Scheduled Fed speakers include Barkin (8am) and Miran (8:30am)

Market Snapshot

- S&P 500 mini little changed

- Nasdaq 100 mini +0.2%

- Russell 2000 mini -0.3%

- Stoxx Europe 600 little changed

- DAX little changed, CAC 40 -0.6%

- 10-year Treasury yield +1 basis point at 4.17%

- VIX +0.3 points at 15.15

- Bloomberg Dollar Index little changed at 1203.74

- euro little changed at $1.1715

- WTI crude +0.2% at $58.43/barrel

Top Overnight News

- China imposed controls on exports to Japan that could have military use, intensifying a dispute between Asia’s top economies over remarks Japanese PM Sanae Takaichi made last year on Taiwan. BBG

- Trump asked Marco Rubio to oversee an economic and political overhaul of Venezuela, leading a team that includes officials working on energy, finance and military police, White House adviser Stephen Miller said. BBG

- In late night Truth Social post, Trump announced that Danish territory is now an American “protectorate.” Denmark and the broader NATO alliance are extremely concerned the US could imminently seize Greenland and paralyze the NATO alliance. The Atlantic

- Trump said he believes the U.S. oil industry could get expanded operations in Venezuela "up and running" in fewer than 18 months. "A tremendous amount of money will have to be spent, and the oil companies will spend it, and then they’ll get reimbursed by us or through revenue," he said. NBC

- Nvidia’s Rubin data-center chips are now in production as strong AI demand drives the need for more powerful systems, CEO Jensen Huang said. Rival AMD unveiled a new AI chip for corporate data-center use. BBG

- Nvidia said it has seen strong demand from customers in China for the H200 chip that the Trump administration has said it will consider letting the chipmaker ship to that country. BBG

- The Trump admin is planning to meet with executives from U.S. oil companies later this week to discuss boosting Venezuelan oil production. The meetings are crucial to the administration's hopes of getting top U.S. oil companies back into the South American nation. RTRS

- MCHP +430 bps in premkt after issuing its second upside preannouncement of the quarter, indicating potential recovery in demand for industrial and automotive chips.

- Trump is scheduled to deliver remarks at a GOP member retreat at 10:00am ET on Tuesday and will participate in a policy meeting at 2:30pm ET.

- Trump posted "Pregnant Women, DON’T USE TYLENOL UNLESS ABSOLUTELY NECESSARY, DON’T GIVE TYLENOL TO YOUR YOUNG CHILD FOR VIRTUALLY ANY REASON, BREAK UP THE MMR SHOT INTO THREE TOTALLY SEPARATE SHOTS". Full post "Pregnant Women, DON’T USE TYLENOL UNLESS ABSOLUTELY NECESSARY, DON’T GIVE TYLENOL TO YOUR YOUNG CHILD FOR VIRTUALLY ANY REASON, BREAK UP THE MMR SHOT INTO THREE TOTALLY SEPARATE SHOTS (NOT MIXED!), TAKE CHICKEN P SHOT SEPARATELY, TAKE HEPATITAS B SHOT AT 12 YEARS OLD, OR OLDER, AND, IMPORTANTLY, TAKE VACCINE IN 5 SEPARATE MEDICAL VISITS! President DJT".

Trade/Tariffs

- China Commerce Ministry imposes export controls on dual-use items to Japan, effective immediately

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were mostly higher following the positive handover from Wall Street, where all major indices gained amid outperformance in energy and a softer yield environment. ASX 200 was the laggard with the index dragged lower by weakness in defensives and the top weighted financial sector, while metal and mining stocks were boosted after the recent climb in underlying commodity prices and reports of an AUD 8.8bln takeover offer for BlueScope Steel. Nikkei 225 rallied at the open to back above the 52,000 level with the advances led by mining and tech-related stocks. Hang Seng and Shanghai Comp conformed to the predominantly upbeat mood, with outperformance in Hong Kong helped by strength in some property names and miners, while aluminium producer China Hongqiao Group led the advances as aluminium prices printed fresh three-year highs.

Top Asian News

- Japan sold JPY 1.96tln 10yr JGB, b/c 3.30x (prev. 3.59x), average yield 2.095% (prev. 1.872%). Lowest accepted price 99.99 vs prev. 98.53. Average accepted price 100.04 vs prev. 98.57. Tail in price 0.05 vs prev. 0.04.

- Japan's nuclear regulator said no irregularities at Chugoku Electric's (9504 JT) Shimane nuclear power plant following the earthquake.

- Earthquake with a preliminary magnitude of 6.3 strikes at the Shimane Prefecture in Japan, according to NIED

European bourses (STOXX 600 U/C) opened with very modest gains, but have indices have since slipped a touch off best levels to show a bit more of a mixed picture in Europe. European sectors are mixed, with Health Care, Energy, and Basic Resource leading. Energy is advancing on higher crude prices, despite the absence of a clear catalyst. On a stock-specific basis, the sector is also being supported by gains in heavyweight names such as Shell (+1.6%) and BP (+1.9%). Meanwhile, sentiment in Basic Resources has been underpinned by strength in metal prices.

Top European News

- 'Coalition of the Willing' to discuss security guarantees for Ukraine

FX

- DXY resides in a narrow 98.161-98.425 range after recovering from worst levels on the back of some EUR softness (more below), although price action across FX thus far has been muted vs other markets (Equities, Fixed Income, Commodities). The US docket for today only consists of S&P Services and Composite Final PMIs alongside commentary from Fed's Barkin and Miran. Perhaps more importantly, US President Trump is due to give remarks later today.

- EUR is on a softer footing, with early weakness commencing shortly after the revisions lower to the French PMIs, whilst downward revisions in German Composite and EZ PMIs further weighed on the single currency. Moreover, German State CPIs were more dovish than the Nationwide figure (at 13:00 GMT) implies. EUR/USD resides towards the bottom end of a 1.1708-1.1743.

- GBP/USD trades flat towards the bottom of a 1.3528-1.3568 range with little immediate move seen on t