Futures Rebound To Session High As Software, Gold And Bitcoin All Jump

US equity futures are poised to open higher with Software companies finally bouncing (as previewed here), even though Amazon continues to be deep in the red after its eye-watering capex outlook. US stocks will cap a bruising week in which a rush to unwind crowded trades – from AI shares to precious metals and crypto – triggered margin calls and amplified the market’s slide. With the S&P 500 on track for its worst week this year, S&P futures are 0.6% higher at 8:15a.m. ET while contracts on the Nasdaq 100, which just suffered its ugliest three days since Trump’s trade war sent markets into a tailspin in April, were up 0.8% after erasing an earlier decline while precious metals and cryptocurrencies climb after falling sharply on Thursday. In premarket trading, Mag 7 are mostly higher except for AMZN which is down -7% post-earnings on a staggering capex guidance ($200BN, vs $146BN est); NVDA +2.7%, MSFT +1.6%. Yields are 1-3bp higher led by the front-end overnight while the USD is at session lows. Commodities are mixed: base metals are lagging, while gold and silver added 2.0% and 4.4%, respectively; oil added 0.4% overnight. Oil trades near session lows as US-Iran nuclear talks take place. Bitcoin has bounced more than 10% from its session lows just above $60K as dip buying makes a tentative comeback.

In premarket trading, Mag 7 stocks are mostly higher with one exception: Amazon is down 7% after the company announced plans to spend $200 billion this year on data centers, chips and other equipment, worrying investors that its colossal bet on artificial intelligence may not pay off in the long run. AI infrastructure stocks rally after Amazon’s massive capex forecast. Gainers include AMD (AMD) +2%. Other Magnificent Seven stocks: Tesla +0.6%, Alphabet -1%, Microsoft +1.3%, Apple -0.4%, Meta Platforms +0.08%

- Cryptocurrency-linked stocks rally as Bitcoin rebounded after a selloff that briefly dragged the token to a more than 50% retreat from its October peak.

- Bill Holdings (BILL) rises 12% after the payments-automation company raised its full-year forecast.

- Bloom Energy (BE) rises 13% after the manufacturer of solid-oxide fuel cells gave a forecast for 2026 revenue that beat the average analyst estimate.

- Hims & Hers Health (HIMS) falls 8% after FDA Commissioner Marty Makary said his agency will take “swift action against companies mass-marketing illegal copycat drugs, claiming they are similar to FDA-approved products.”

- Impinj (PI) falls 27% after the semiconductor device company gave an outlook that is much weaker than expected, given an inventory overbuild. The results prompted a downgrade

- Molina (MOH) tumbles 25% after the health insurer forecast 2026 profit that was less than half of Wall Street’s expectations.

- Reddit (RDDT) climbs 8% after the social-media company’s fourth-quarter results beat expectations across key metrics. It also gave an outlook that is seen as strong.

- Roblox (RBLX) jumps 8% after the video-game company reported fourth-quarter results that beat expectations on key metrics. It also gave an outlook that is seen as positive.

- Stellantis (STLA) plunges 27% after the carmaker said a business reset resulted in charges of around €22.2 billion for the second half of 2025. Akros says the charges were about double what they expected.

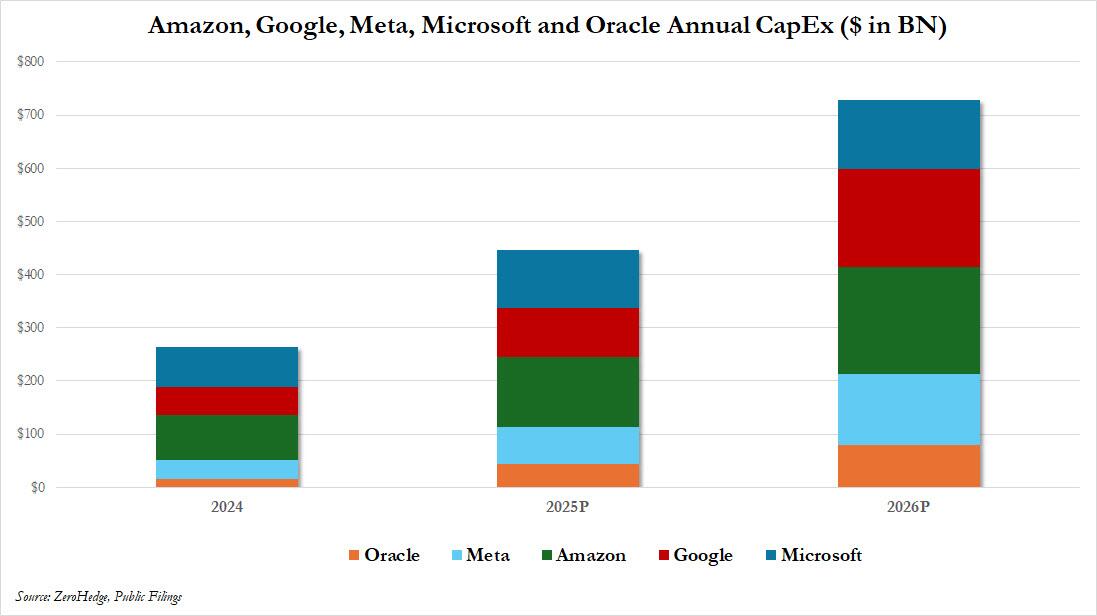

Investors have been spooked by developments on two fronts: the rollout of models from AI startup Anthropic that threaten to render large swaths of software services redundant, alongside the eye-watering spending plans of tech companies. Four of the biggest tech firms plan to invest around $650 billion this year in data centers and the equipment required to run them.

Amazon, almost 8% lower in pre-market trading, is the latest Mag7 member to spook investors about ballooning AI spending, projecting $200 billion for capex this year, far more than the $146 billion Wall Street had penciled in. Taken together with plans from Meta, Google and Microsoft, capital spending by the Big Four AI “hyperscalers” is set to hit about $650 billion this year — up from $356 billion in 2025 and under $100 billion in 2020. On current trajectories, that suggests the quartet’s capex could top $1 trillion in 2027, a scale of investment that’s giving investors pause in what has long been a disinflationary tech industry.

Some investors still appear willing to open their wallets. Oracle’s record-setting bond deal on Monday is an encouraging signal for other big tech firms seeking to raise hundreds of billions of dollars for data-center infrastructure, according to Goldman Sachs’ syndicate desk. Yet if the mounting cost of building AI is rattling markets, so too is the disruption the technology threatens to unleash on other industries. Anthropic is rolling out a new model, Claude Opus 4.6, tailored for financial research – just days after its move into legal services jolted legacy software providers. Meanwhile, Blackstone-backed Liftoff Mobile postponed its IPO this week as a selloff in tech shares compounded investor concerns about AI’s impact.

Still, the week’s retreat is allowing traders to separate stocks facing genuine risk or overvaluation from those caught up in the broader risk-off rout, as the AI rally of the past three years continues to broaden beyond the largest names.

“This is an opportunity for us as active investors to take the baby that has been thrown out with the bath water, because there’s still names out there that we believe will come out very well,” said Fabiana Fedeli, chief investment officer for equities, multi-asset and sustainability at M&G Investments.

For Rory Sandilands, a fixed-income portfolio manager at Aegon Ltd., uncertainty over the disruptive nature of AI may linger as it remains too early to tell how effective the new tools are, or how quickly other software may become obsolete.

“What we’re seeing in the marketplace is fear, because nobody understands really who the winners and losers will be,” Sandilands said. “There’s not enough cushion in credit spreads in aggregate to really to help soften that blow.”

Bitcoin, another canary in the coal mine for risk appetite, touched a new 15-month low of $60,033 on Friday morning, before rallying more than 10%. The original cryptocurrency suffered its biggest daily drop since 2022 on Thursday. Bitcoin’s plunge is intensifying the crisis rocking the digital-asset complex. Few companies are more exposed than Strategy, which confirmed in earnings announcement on Thursday a net loss of $12.4 billion for the fourth quarter, driven by the mark-to-market decline in its vast holdings. Retail investors who piled into the Trump administration’s promised crypto paradise via Wall Street-approved funds are also learning an expensive lesson in market gravity. Crypto funds had their biggest outflows since November in the week ended Feb. 4, Bank of America says, citing EPFR Global data. Money market funds attracted the most inflows, along with stocks. That said, today crypto may finally be due for a rebound: tracking the Software basket, bitcoin is more than 10% above the overnight lows of $60K, trading near session highs of $67K.

Silver has managed a modest rally from Thursday’s 17% leg lower, but remains nearly 39% down from its peak barely a week ago.

Also recall: it may be the first Friday of the month, but there are no non-farms payrolls. Earlier this week, the Bureau of Labor Statistics said the January jobs report would be delayed to next Wednesday because of the partial government shutdown.

Turning to earnings, companies representing nearly 70% of the S&P 500’s market value have now reported in this earnings season. Of the 289 S&P 500 companies to have reported so far, more than 78% have beaten analysts’ forecasts, while 17% have missed. Next week, the calendar is much lighter, with another 8% of the S&P’s market cap reporting. Philip Morris International and Biogen are among those companies expected to report results before the market opens on Friday. PMI investors will be looking for continued strength in its smoke-free portfolio, which includes heated tobacco products and nicotine pouches, to support high-single digit sales growth in the fourth-quarter. For Biogen, all eyes will be on the performance of Leqembi, the drugmaker’s treatment for early Alzheimer’s disease.

European stocks also advance, with construction, utility and bank shares leading gains. Autos underperform as Stellantis shares tumble. Consumer products and chemicals also lag, while construction shares outperform, as French group Vinci announced strong 2025 earnings. Here are some of the biggest movers on Friday:

- Bayer rises as much as 3.2% after the German company said its experimental drug — called asundexian — cut the risk of secondary strokes by 26% in a late-stage trial.

- Kongsberg shares soar as much as 17% after the Norwegian defense firm posted results that Morgan Stanley says delivered a strong end to the year, with all divisions recording double-digit growth in the fourth quarter.

- Vontobel shares rise as much as 6.1% after the investment management firm reported a significant trading-driven earnings beat, according to analysts at Citi.

- Renk Group shares rise as much as 10% after BNP Paribas raises its recommendation on the German defense company to outperform from neutral, citing a reassuring message from the CEO over the upcoming earnings report and the outlook for 2026.

- Stellantis shares fall as much as 24%, the steepest drop on record, after the carmaker said a business reset resulted in charges of around €22.2 billion for the second half of 2025. Akros says the charges were about double what they expected.

- SocGen shares dropped as much as 4.1% following a strong rally after the French lender reported what an RBC analyst says are mixed results as Bloomberg Intelligence notes trading revenue missed estimated and fell short of peers.

- Kering shares fall as much as 5.5% after Morgan Stanley trimmed its price target on the French luxury group ahead of next week’s earnings, saying recent channel checks point to a more difficult start to 2026 than anticipated.

- Coloplast shares drop as much as 9.6% after the Danish medical products-maker reported weaker-than-expected sales and earnings for the first quarter, hurt by its Kerecis skin substitutes business.

- Anglo American shares fall as much as 3.1% after BofA analysts cut the miner’s rating to neutral from buy, citing risks to completing its Teck Resources acquisition and uncertainty over the value of non-core businesses.

- European software and IT services stocks are coming under renewed pressure, tracking declines in Asian and US peers, after Anthropic unveiled a new version of its most powerful artificial intelligence model designed to carry out financial research.

Earlier in the session, Asian stocks pared their initial declines on Friday but still headed for a weekly slide, dragged by concerns over artificial intelligence shares and panic selling in precious metals. The MSCI Asia Pacific Index dropped as much as 1.3% before trading little changed in Friday’s session, with South Korea and Taiwan’s tech-sensitive markets overcame declines. Stocks in Hong Kong dropped and mainland China extended its retreat, while Japan’s market rebounded after opening at a loss. On the week, the regional gauge slid as much as 2.5%, set to snap its streak of advances that started in mid-December. Thailand will also be heading to the polls for a general election, with spending plans and measures to support growth among investors’ top priorities. Shares in India were steady after the central bank kept its benchmark interest rate unchanged, signaling an end to its easing cycle.

“Asian markets have fallen this week as volatility in precious metals prompted investors to reassess stretched valuations more broadly,” said Fabien Yip, market analyst at IG International. A spillover from the US tech selloff has added more pressure, although the region’s decline has been more moderate than global peers, she added.

In FX, the Bloomberg Dollar Spot Index is down 0.2% while the Norwegian krone and Australian dollar are the best performing G-10 currency, rising 0.8% each against the greenback. USD/JPY is little changed ahead of the Japanese election on Sunday.

In rates, treasuries edge lower, pushing US 10-year yields up 2 bp to 4.20%. Gilts lead a rally in European government bonds, with UK 10-year yields falling 3 bps to 4.53%. A combination of the Trump administration’s focus on affordability and a weakening employment picture could open the door to further rate cuts, said Mohit Kumar, chief strategist for Europe at Jefferies.

“Our view remains that we could get a scenario where growth is robust and yet employment is weakening due to the impact of AI,” Kumar wrote. “A Warsh-led Fed could end up being more dovish than what the market currently expects.”

Money market funds attracted the most inflows in the week ended Feb. 4 along with stocks, Bank of America Corp. said, citing EPFR Global data. Crypto funds had their biggest outflows since November, while gold funds saw their first weekly outflow since November.

In commodities, WTI crude futures are steady near $63.30 a barrel as traders eyed the outcome of talks between Iran and the US. Spot silver rises over 5% while Bitcoin rallies back above $66,000 after dropping more than 50% from its October peak.

Looking at today's calendar, the University of Michigan’s provisional reading of consumer sentiment in February is due at 10 a.m. ET however.

Market Snapshot

- S&P 500 mini +0.4%

- Nasdaq 100 mini +0.5%

- Russell 2000 mini +0.8%

- Stoxx Europe 600 little changed

- DAX +0.1%

- CAC 40 -0.2%

- 10-year Treasury yield +1 basis point at 4.19%

- VIX -1.3 points at 20.51

- Bloomberg Dollar Index -0.1% at 1193.65

- euro +0.1% at $1.1794

- WTI crude +0.7% at $63.73/barrel

Top Overnight News

- Oil dropped US-Iran talks got underway in Oman, with Tehran indicating that a quick deal is unlikely. BBG

- The U.S. Virtual Embassy in Iran issued a security alert early Friday urging American citizens to “leave Iran now.” The notice came as American and Iranian officials were scheduled for a new round of negotiations in Oman on Friday. CNBC

- Bitcoin is bouncing this morning (currently +525bps), rising after a selloff that briefly dragged the token to more than 50% below its October peak. BBG

- US consumer sentiment probably edged lower at the start of February on concerns about a cooling labor market and elevated prices. BBG

- BOJ board member Kazuyuki Masu highlighted the need for a higher benchmark interest rate. BBG

- Indonesia’s assets slid after Moody’s cut the country’s credit outlook to negative. The cost of insuring sovereign debt rose to around 80 bps, the biggest increase among Asian sovereigns. BBG

- Intel and AMD have notified Chinese customers of supply shortages for server central processing units (CPUs), with Intel warning of delivery lead times of up to six months. The supply constraints have driven up prices for Intel's server products in China by more than 10% generally, although pricing varies by customer contract. RTRS

- Big Tech stocks sold off heavily after the companies unveiled plans to spend $660bn this year on AI, as investors fret that the “breathtaking” capital expenditures are outpacing the eranigns potential of the new technology. Amazon, Google and Microsoft are set to lose a combined $900bn in mkt value since filing their quarterly earnings over the past week. FT

- Sweden’s core inflation slowed more rapidly than expected last month, suggesting a March rate cut may be in play. The CPIF rate excluding energy fell to 1.7% from 2.3% in December. BBG

- South Korean official said US is taking necessary steps regarding the issue of South Korea being on sensitive country lists: Yonhap.

Trade/Tariffs

- Japan and US 1st round of investment to include gas power, ports and artificial diamond, totalling JPY 6-7tln, Nikkei reported.

- Chinese Commerce Ministry said they will lead policy measures to promote travel service exports and boost inbound consumption.

- French President Macron to visit Japan at the end of March, via Nikkei.

- South Africa Trade Minister said they signed a framework economic partnership with China, while the agreement will be followed by an early harvest agreement by end of March 2026, which will then see China provide duty-free access to South African exports.

- South Korea Foreign Minister said South Korea is not intentionally delaying US investment.

- Venezuela and Qatar review bilateral agenda to strengthen cooperation.

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were ultimately mixed after the global market rout rolled over into the region following the continued tech woes stateside and weak US labour market data. Nonetheless, most of the regional benchmark indices are well off their worst levels, as the early sell-off gradually stabilised. ASX 200 was among the underperformers with the index dragged lower by heavy tech losses, and with sentiment also not helped by M&A-related disappointment after the proposed Rio Tinto-Glencore merger fell through, while there were comments from RBA Governor Bullock, who noted the RBA board is not happy with inflation and the prospects of getting it down. Nikkei 225 initially declined amid the broad risk-off mood and disappointing Household Spending data, but then recovered as sentiment improved and with participants awaiting the snap election on Sunday, where the ruling bloc is widely anticipated to achieve a landslide victory. Hang Seng and Shanghai Comp were mixed amid a lack of fresh pertinent catalysts and with the mainland clawing back all of its early losses following another two-pronged liquidity operation by the PBoC utilising both 7-day and 14-day reverse repos.

Top Asian News

- Indonesian President said they signed a security treaty with Australia.

- Former Bank of China (3988 HK) Vice President was expelled from the China Communist Party for serious violations of discipline and law.

- China's Ministry of Agriculture issues implementation plan to advance rural revitalisation and agricultural modernisation.

- Japan ruling parties expected to win over 300 seats out of the 46