Futures Plunge As German Bond Rout Goes Global

Futures tumble, led by Tech as the world is hammered by soaring yields from Europe to Japan. As of 8:00am ET, S&P futures are down 1.1%, and Nasdaq futures plunged 1.4% as Marvell Technology shares were among the biggest premarket losers, dropping about 15%, after the chipmaker’s result and revenue forecast failed to live up to investors’ lofty expectations. MongoDB Inc. dropped 17% after the database software company gave a disappointing forecast. Mag 7 underperform: NVDA (-1.8%), TSLA (-1.6%) and META (-1.5%) pre-market. 10y yields are +2bps higher while 2y is -1.5bp lower this morning but the move is nothing compared to Germany where yields earlier soared as much as 15bps (they have since retraced much of the move) extending yesterday's record rout; the USD plunge continues, just as Bessent wanted, with the rest of the world about to find out what soared trade deficits really mean. Commodities are mixed: oil saw small gains (+0.5%) after yesterday’s selloff; basic metals are rallying this morning, while precious metals are lower. Since yesterday’s close, the equity weakness was not contributed by single catalyst but more due to a number of macro uncertainties (the auto tariffs delay will not resolve the tariffs risks; more evidence of sentiment impacts from Beige book) and rotation to international stocks. Today, we will hear from AVGO on AI outlooks; MRVL fell -15% post earnings release yesterday (after-market) despite numbers are mostly in line with expectation.

In premarket trading, Tesla and Nvidia fall more than 2% are leading premarket losses among the Magnificent Seven stocks on Thursday. Amazon, Microsoft, Alphabet, Meta and Apple fall less than 1%. Burlington Stores (BURL US) shares rise 14% in premarket trading after the retailer reported fourth-quarter comparable sales and profit that topped Wall Street expectations. Still, its annual forecasts fell short, with Chief Executive Officer Michael O’Sullivan saying the outlook for 2025 is “very uncertain.” Here are the other notable premarket movers:

- ALX Oncology (ALXO US) shares rise 13% in premarket trading after Jefferies upgraded the drug developer to buy from hold, citing “limited theoretical downside.”

- CoreCivic Inc. (TH US) will resume operations at the South Texas Residential Center under an amended intergovernmental services agreement (IGSA).

- JD.com ADRs (JD US) jump as much as 11% in premarket trading on Thursday after the Chinese e-commerce firm reported net revenue for the fourth quarter that beat the average analyst estimate. Peers PDD Holdings climbs 4.4% and Alibaba Group rises 3.8%. .

- MongoDB shares (MDB US) are down 18% in premarket trading Thursday, after the database software company gave a full-year forecast that is weaker than expected.

- ON Semiconductor (ON US) analysts are generally positive on the company’s bid to buy Allegro Microsystems (ALGM US), seeing synergies between the two, though some questioned the offer price, which values the company at $6.9 billion including debt.

- Shares of ECARX Holdings (ECX US), a mobility technology provider, are up 9.1% in premarket trading after the company said it won an award to provide Volkswagen and Skoda with digital cockpit solutions.

- Victoria’s Secret (VSCO US) shares fall as much as 2.7% in US premarket trading after the lingerie retailer’s forecasts for the first quarter and for the full year fell short of analyst expectations with the company citing an uncertain backdrop and shift in consumer confidence. Analysts at BMO and JPMorgan cut their price targets on the stock.

Chip shares came under renewed pressure after Alibaba Group Holding Ltd. introduced its Qwen platform, a model that it claims performs as well as Chinese start-up DeepSeek but with a fraction of the data. The news, alongside the underwhelming earnings, are denting investor confidence in US companies’ dominance in AI.

“Clearly Alibaba is weighing on sentiment,” said Alexandre Hezez, chief investment officer at Group Richelieu in Paris. “The tech sector has been weakened lately, if you combine that with Marvell, it’s a pretty sour cocktail for US stocks”

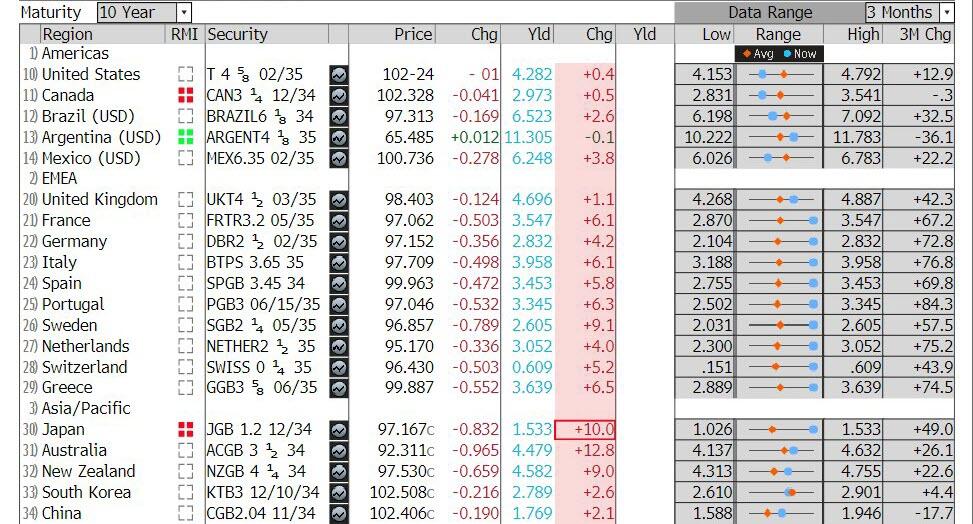

Europe’s Stoxx 600 index slipped 0.6%, as real estate and consumer product names underperform, reacting to sharply higher bond yields across the continent, following Germany’s announcement earlier this week that it would deploy hundreds of billions of euros in additional spending. Indeed, German government bonds fall again, extending their worst daily drop since 1990 and pushing 10-year yields up another 6 bps to 2.85%. And this time the selling has spilled over across Europe and is also hammering Japan.

Auto shares bucked the trend, however, after President Donald Trump offered the sector a one-month reprieve from the tariffs levied on Mexican and Canadian imports. The DAX is up 0.4% as bonds sell off across the world. Automakers extend rally following a delay in some US tariffs on Mexico and China. Focus is also on the European Central Bank meeting later Thursday. Here are some of the biggest movers on Thursday:

- German stocks touched a record high, rising for a second day after chancellor-in-waiting Friedrich Merz said that the country would unlock hundreds of billions of euros for defense and infrastructure investments. Meanwhile, news that the US will delay Canadian and Mexican tariffs on automakers for a month also boosted German car companies.

- Lufthansa shares rise as much as 9.1%, the biggest jump since March 2022. The German flag carrier reported a return to adjusted Ebit growth in the fourth quarter and guided a “significant” increase in 2025.

- Air France-KLM shares soar as much as 20%. Strong unit revenues drove a fourth-quarter Ebit beat, while management commentary that operating profit guidance for fiscal year 2025 would be at least €300 million higher than the previous year across the business reassured the market.

- Deutsche Post advances as much as 13% following fourth-quarter results that saw a strong performance from the company’s Express unit.

- Kenmare shares jump as much as 52%, the most since 2015, after the titanium minerals company said it rejected a takeover offer tabled by a consortium that includes its former managing director Michael Carvill.

- JCDecaux shares rise as much as 20%, the most since November 2020, as results and guidance from the French outdoor advertising firm were met with an outpouring of relief.

- European real estate and utility stocks are underperforming again on Thursday as a global bond selloff continued due to Germany’s spending plans, with investors looking ahead to the European Central Bank’s interest-rate decision later today.

- Spire Healthcare falls as much as 25% as the UK hospital operator’s full-year guidance misses analyst estimates.

- Galderma shares drop as much as 9.3%, the most on record, after the Swiss skincare company forecast “clearly subdued” net sales growth in the first quarter from a year earlier due to phasing.

Germany’s spending plan drove Bunds on Wednesday to their worst session since 1990 and the selloff extended on Thursday. The moves rippled into markets across the euro area and beyond, with Japanese 10-year borrowing costs earlier reaching the highest in over a decade and Treasury yields rising three basis points.

Investors are now waiting for the European Central Bank’s meeting, which is expected to deliver a 25 basis-point interest rate cut, and could yield clues on how rate-setters might react to the additional spending plan.

“This is ultimately a reassessment of the reality that Europe needs to find some financing,” Rabobank strategist Matthew Cairns said of the bond selloff. “Some more repricing is likely, then the ECB will come in and attempt to settle market sentiment.”

Earlier in the session, Asian stocks rose as Chinese shares extended their rally and Donald Trump exempted automakers from newly imposed tariffs on Mexico and Canada for one month. The MSCI Asia Pacific Index rose as much as 1.5%, set for second day of gains, with Alibaba among the biggest boosts after unveiling its latest AI model. Hong Kong’s Hang Seng Index led advances, rising 3.3%. Stocks also climbed in mainland China, Japan and South Korea. Ongoing anticipation of further stimulus as well as vows to support the development of new technologies such as AI are powering China’s rally after the nation set bullish growth targets for the year at the start of the National People’s Congress on Wednesday. While China’s ambitious goals signal its preparedness for a looming trade war, investors remain cautious on the sustainability of share-price gains amid increasing geopolitical uncertainty. Elsewhere, Japanese stocks climbed on boosts from the US tariff delay as well as Germany’s historic spending plans. Malaysian equities slipped ahead of an interest rate decision, with the central bank standing pat as expected.

In FX, the euro is little changed just below $1.08 ahead of the European Central bank decision, having ventured above that level earlier.

In rates, treasuries are mixed as US trading gets under way with belly to long-end yields higher on the day while front end outperforms, leaving 2s10s spread near widest levels of past month. France and Germany lead bigger selloff in core European rates, weighing on Treasuries and extending this week’s global yield-curve steepening move. US 10- to 30-year yields are more than 3bp higher on the day with 2-year little changed, leaving 2s10s near 32bp, last seen Feb. 4; German 10-year adds more than 6bp to Wednesday’s 30bp surge, French 10-year is 8bp higher after rising 26bp.Focal points of US session include weekly jobless claims data and three Fed speakers, following ECB rate decision at 8:15am New York time; President Christine Lagarde speaks 30 minutes later. German government bonds fall again, extending their worst daily drop since 1990 and pushing 10-year yields up another 6 bps to 2.85%. And this time the selling has spilled over across Europe and is also hammering Japan.

In commodities, oil prices advance, with WTI up 0.5% near $66.60 a barrel. Spot gold falls $20 to around $2,898/oz. Bitcoin rises 1% and above $91,000.

The US economic data calendar includes February Challenger job cuts (7:30am), January trade balance, 4Q final productivity and unit labor costs, and jobless claims (8:30am) and January wholesale trade sales (10am). Fed speaker slate includes Harker (8:45am), Waller (3:30pm) and Bostic (7pm)

Market Snapshot

- S&P 500 futures down 1.0% to 5,794.50

- STOXX Europe 600 down 0.2% to 554.81

- MXAP up 1.5% to 189.77

- MXAPJ up 1.2% to 594.54

- Nikkei up 0.8% to 37,704.93

- Topix up 1.2% to 2,751.41

- Hang Seng Index up 3.3% to 24,369.71

- Shanghai Composite up 1.2% to 3,381.10

- Sensex up 0.9% to 74,375.12

- Australia S&P/ASX 200 down 0.6% to 8,094.71

- Kospi up 0.7% to 2,576.16

- Brent Futures up 0.5% to $69.65/bbl

- Gold spot down 0.7% to $2,900.07

- US Dollar Index little changed at 104.21

- German 10Y yield little changed at 2.86%

- Euro little changed at $1.0789

- Brent Futures up 0.5% to $69.64/bbl

Top Overnight news

- US President Trump said he is collaborating with House Republicans on a Continuing Resolution to fund the government through September. It was separately reported that Trump is expected to issue an executive order as soon as Thursday aimed at abolishing the Education Department, according to WSJ.

- The Trump administration is weighing more exemptions from the new tariffs on Canada and Mexico — this time for the agriculture industry. Officials are discussing waiving the 25 percent duty on some agriculture products, including Canadian potash, a key ingredient in fertilizer. Politico

- Trump executive order could be released as soon as Tues calling for the Dept. of Education to be abolished (although doing so would require an act of Congress). WSJ

- Walmart Inc. has asked some Chinese suppliers for major price reductions, with the US retail giant’s efforts to shift the burden of President Donald Trump’s tariffs facing strong pushback from firms in the Asian nation, according to people familiar with the matter. Some suppliers, including producers of kitchenware and clothing, have been asked to lower their prices by as much as 10% per round of tariffs, essentially shouldering the full cost of Trump’s duties. BBG

- New York Fed's Perli said balance sheet drawdown has been smooth and financial system reserves remain abundant but flagged the challenge of managing balance sheet cuts amid debt ceiling debate. Perli added that the Fed’s reverse repos can likely shrink further and the Fed may bring back early morning SRF operations at quarter-end.

- BofA card spending (March 1st): 1.4% Y/Y (1.9% January average), spending growth -0.3%

- Germany’s “fiscal bazooka” is positive for the country’s AAA credit rating according to S&P as Berlin has plenty of capacity for higher spending levels and will see a benefit to growth from the move. RTRS

- China is considering scrapping a price cap for local governments buying unsold apartments to help clear of millions of empty homes, people familiar said. Property stocks extended gains. BBG

- South Korea’s CPI for Feb comes in a bit below expectations, including headline +2% (down from +2.2% in Jan, and below the Street’s +2.1% forecast) and core +1.8% (down from +1.9% in Jan, and below the Street’s +1.9% forecast). BBG

- Japan’s biggest union group demanded an average wage hike of 6.09% this year, the most since 1993, signaling the kind of sustainable pay growth that may help drive the economy. BBG

- President Emmanuel Macron has said he will hold talks with allies over how France’s nuclear weapons could protect Europe, as the continent steps up efforts to guard against an emboldened Russia. Macron responded to a call by Germany’s Merz about whether France and the UK would be willing to do some sort of “nuclear sharing” if US became less reliable partner. FT

- The ECB is expected to cut rates by a quarter-point to 2.5% but focus will be on the outlook. Beyond today, opinions vary with one analyst seeing no more reductions while others reckon the benchmark will go down to 1% in early 2026. BBG

A more detailed look at global markets courtesy of Newsquawk

Russian Foreign Minister Lavrov says a "solution in Ukraine is possible within weeks if the West stops supporting Kiev", via Sky News Arabia. Ukrainian President Zelensky anticipates positive outcomes from US cooperation next week. It was also reported that Zelensky’s top aide discussed with the US National Security Advisor steps to achieve just peace, while Ukraine and the US agreed on a meeting in the near future. Four senior members of Trump's entourage have held secret discussions with some of Kyiv’s top political opponents to Ukrainian President Zelensky, according to Politico.

Top Asian News

- PBoC Governor Pan says they will study, establish new structural policy tools, will cut interest rates and Bank's RRR at appropriate time. Wil prevent FX rate overshooting risks. Will roll out tech board on the debt market. Will expand relending facility for tech sector. Will expand relending facility from CNY 500bln to CNY 800bln-1tln.

- Rengo, Japan's largest labour union, is seeking a wage hike of 6.09% for 2025 (sought 5.85% in 2024)

- A team from China recently unveiled its general-purpose AI Agent product, Manus, which is said to outperform the OpenAI model of the same level, according to Shanghai Securities News.

- China's State Planner, on the 2025 GDP target, says external uncertainties are increasing and domestic demand is not sufficient; complete confidence in attaining the growth target.

- China's Finance Minister, on fiscal policy, says China has ample policy room in the scenario of possible uncertain factors bother external and internal.

European bourses (STOXX 600 -0.5%) opened with a clear positive bias, but as the morning progressed, indices gradually drifted lower to display a more negative picture in Europe. European sectors are mixed vs initially opening with a positive bias. Autos is the clear outperformer today with optimism stemming from the White House, which said it will give one month exemptions on any autos coming through USMCA; Stellantis (+2.3%), Porsche AG (+2%). Real Estate is once again towards the foot of the pile, as yields continue to tick higher in the fall out from Germany’s spending plans. US equity futures are entirely in the red, with clear underperformance in the tech-heavy NQ (-1.2%); sentiment for the index is hit following Marvell results; the co. beat on headline metrics but its Q1 guidance disappointed – shares are lower by 15% in pre-market trade.

Top European News

- Goldman Sachs expects the ECB's benchmark interest rate to reach 2% by June 2025 but no longer expects a 25bps cut in July. Goldman Sachs raised Germany's 2025 economic growth forecast by 0.2 percentage points to 0.2% citing higher public spending on defence and infrastructure and raised the euro area's 2025 economic growth forecast by 0.1 percentage point to 0.8%, while it sees some spillovers from Germany into neighbouring countries and now expects the rest of the euro area to step up military spending somewhat more quickly in response to the German shift.

- BoE Monthly Decision Maker Panel data – February 2025. Expectations for CPI inflation a year ahead rose from 3.0% to 3.1% in the three months to February. The corresponding measure for three-year ahead CPI inflation expectations was 2.8% in the three months to February, which was unchanged from the three months to January. Expected year-ahead wage growth remains unchanged at 3.9% on a three-month moving-average basis in February.

- Germany's lower house to start discussing debt brake reform on March 13, via Reuters citing sources; to vote on debt brake reform on March 18.

- Turkish CBT Weekly Repo Rate (Feb) 42.5% (Prev. 45.0%)

FX

- DXY remains pressured and has extended its losing streak to a fourth session in a row. Recent price action has largely been a EUR story which has had a mechanical impact on the USD, with the JPY today also acting as a drag. From a US lens, this week has been characterised by soft US data and tariff angst given actions taken earlier in the week. From a US lens, this week has been c