The first quarter of 2025 has bucked expectations of a “Trump trade.” Contrary to what many anticipated, U.S. President Donald Trump’s return to office hasn’t been smooth sailing for markets. Back-and-forth tariff threats on key trade partners like Canada and Mexico have created uncertainty for investors, contributing to market volatility.

Year to date, as of March 17, the S&P 500 is down 3.8%, while the tech-heavy Nasdaq 100 has slid even further, dropping 6.5%.

With stocks struggling, you might be eyeing bond exchange traded funds (ETFs) as a refuge from equity risk and a way to diversify a mostly equity portfolio. A popular choice is the BMO Aggregate Bond Index ETF (ZAG)—a diversified option with a low 0.09% management expense ratio (MER).

Did you know these types of bond ETFs aren’t as safe as they appear? Conventional wisdom says bonds offer lower risk and lower returns than stocks, but there are nuances to this rule that most investors overlook when they’re packaged into an ETF.

Here’s what you need to know about how broad bond ETFs like ZAG actually fare under market stress, and my preferred alternative for diversifying a portfolio.

Tools

MoneySense’s ETF Screener Tool

Understanding credit risk with bond ETFs

All bonds carry some degree of credit risk, which is the possibility that the issuer could default on paying you back. In the bond market, credit quality is generally sorted into two broad categories:

- Investment-grade bonds (rated BBB and above)

- Non-investment-grade bonds (aka junk bonds or high-yield bonds)

The highest rating is AAA, which represents the safest, most creditworthy issuers, while BBB-rated bonds sit at the lowest rung of investment grade.

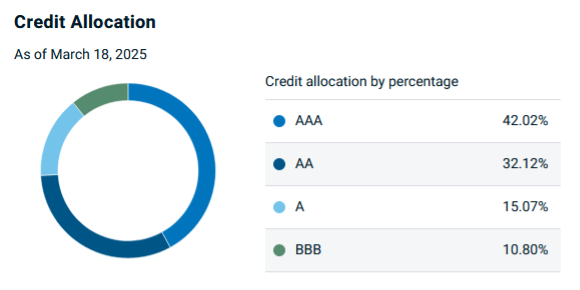

So-called “aggregate” bond ETFs like ZAG target an overall portfolio quality of investment grade—so a minimum of BBB, but often much higher. For example, ZAG tracks the FTSE Canada Universe Bond Index, which consists of a mix of federal, provincial and corporate bonds.

As of March 18, ZAG’s credit quality breakdown is as follows:

Here’s the issue: During times of extreme market stress, the corporate bond portion—largely BBB-rated bonds—can see their value drop sharply and become illiquid.

Why does this matter for ETFs? During March 2020’s COVID crash, we saw panicked posts from investors on Reddit like:

ZAG crashing hard today -9%

byu/dakedenizen inCanadianInvestor

Why did some bond funds crash?

ETFs use an “in-kind” creation/redemption process to keep their market price aligned with their net asset value (NAV). When investors buy or sell ETF units, authorized participants (APs)—typically large institutions like banks or market makers—either create new ETF units by purchasing the underlying bonds or redeem shares by selling them back into the market.

When the market gets chaotic, over-the-counter traded corporate bonds can become even more illiquid than usual—especially compared to stocks, which trade on exchanges, and government bonds, which trade in high volumes. This matters because APs rely on sourcing these bonds for in-kind creations and redemptions of ETF shares. When corporate bonds become illiquid, it gets harder to price them accurately, and the ETF’s market price can deviate significantly from NAV.

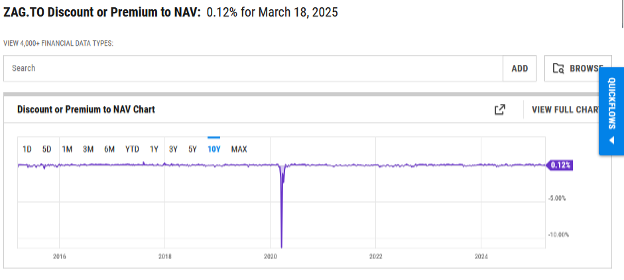

As a result, during the height of the March 2020 panic, ZAG’s market price actually traded at an extreme discount to NAV, as deep as -11.3%.

If you were holding ZAG as a safe refuge, and planned to buy the equities dip, this wouldn’t have worked because you would have had to sell at a steep discount just to exit. ZAG wasn’t the low-risk ballast many investors assumed it would be. Yes, the discount to NAV reversed quickly within days, thanks to rapid government stimulus that stabilized the market. But the COVID-19 crash was short-lived. Who knows what the next crisis will look like?

If corporate bond markets freeze up again, you could see the same liquidity issues. And if that happens, a broad bond ETF like ZAG may not provide the safety you’re counting on.

Rankings

The best ETFs in Canada

How to avoid a bond-market freeze

Personally, for my bond allocation, I’ve discarded aggregate bond ETFs like ZAG entirely and rely exclusively on government-issued bonds. For myself, with a U.S. dollar-dominant portfolio, that means U.S. Treasuries. But for Canadians investing in Canadian dollars, a solid alternative is the iShares Core Canadian Government Bond Index ETF (XGB), which tracks the FTSE Canada All Government Bond Index.

XGB only holds federal and provincial bonds, with no corporate exposure. The MER remains reasonable at 0.12%, and while you lose some yield versus ZAG, you gain much higher safety. For me, the point of holding bonds in a portfolio isn’t income; it’s diversification and drawdown protection.

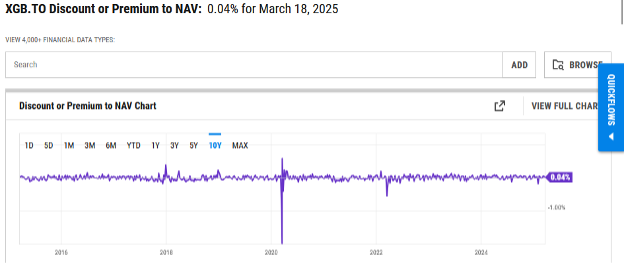

During the March 2020 COVID-19 sell-off, XGB held up significantly better than ZAG. The maximum discount to NAV it reached was just -2%, compared to ZAG’s -11.3%. That’s a huge difference if you actually needed to sell bonds to rebalance into stocks at the time.

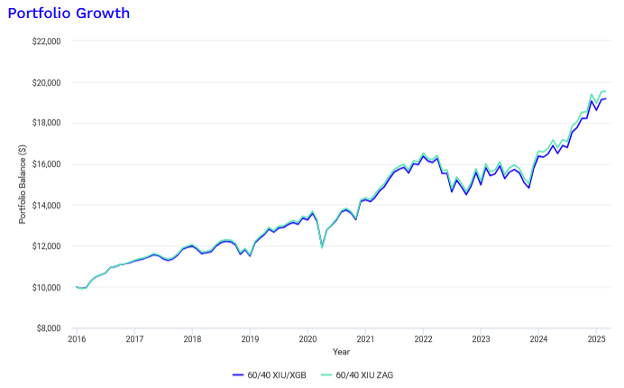

Moreover, as shown in the following back test, a 60% allocation to the iShares S&P/TSX 60 Index ETF (XIU) and 40% in XGB, rebalanced quarterly, has still delivered very similar total and risk-adjusted returns compared to a 60/40 XIU/ZAG portfolio—but without the added credit risk.

Portfolio performance statistics

| Metrics | 60/40 XIU/XGB | 60/40 XIU ZAG |

|---|---|---|

| Start balance | $10,000 | $10,000 |

| End balance | $19,179 | $19,536 |

| Annualized return (CAGR) | 7.36% | 7.58% |

| Standard deviation | 8.68% | 8.88% |

| Best year return | 15.37% | 15.69% |

| Worst year return | -8.53% | -8.26% |

| Maximum drawdown | -12.04% | -13.07% |

| Sharpe ratio | 0.62 | 0.64 |

| Sortino ratio | 0.95 | 0.96 |

If you think like I do—that bonds are for safety and ballast for rebalancing a diversified portfolio—there’s little incentive to hunt for extra yield with corporate bonds. In my view, corporates are best suited for income investors, not those focused on total return.

Newsletter

Get free MoneySense financial tips, news & advice in your inbox.

Read more about ETF investing:

- How to stay invested in U.S. stocks without the tech overweight

- ETF strategies to help Canadian investors combat a weak loonie

- Questrade trading fees: Good news for Canadian investors

- Buying China ETFs in Canada: Is it worth it?

The post Is your bond ETF actually a safe investment? Here’s how to check appeared first on MoneySense.