UBS Says Soaring Memory Chip Prices To "Turbo-Charge" Samsung Earnings

For several months, we have tracked a sharp increase in DDR5 DRAM pricing, as evidenced by DRAMeXchange data, driven primarily by surging AI-related cloud computing demand and hyperscalers accelerating data center buildouts.

On day one of the new year, Samsung co-CEO Jun Young Hyun told employees in an internal memo that customers have praised the differentiated competitiveness of its next-generation high-bandwidth memory (HBM) chips, or HBM4, saying, "It's even earning an assessment from customers that 'Samsung is back'." He noted that Samsung will also benefit from favorable memory market conditions this year, as demand for artificial intelligence chips has materialized much quicker than initially anticipated.

The other week, Goldman analyst Maho Kamiya told clients that mounting concerns about soaring memory prices posed new risks for Nintendo, which manufactures consumer electronics such as the popular Switch 2.

"Some investors think that Nintendo will be selling Switch 2 at a loss and gross profit falling into the red. While rising memory prices are a risk factor that could depress hardware margins, we think concerns are somewhat excessive," Kamiya told clients last week.

While end-use consumer electronics companies such as Nintendo may be pressured by higher memory costs, the same pricing surge is expected to "turbo-charge earnings" for Samsung's memory business, according to UBS analyst Nicolas Gaudois.

Gaudois explains why:

DDR and NAND contract pricing coming out higher than expected

With 4Q25 memory contract pricing negotiations now completed, we lift our forecast for DDR contract pricing to +35% QoQ (was +21%), and for NAND +20% (was +15%). We believe customers are trying to secure 1Q26 contract pricing in earnest, with further potential for upside. We now forecast blended DDR contract pricing to increase 29% QoQ (was +15%) and NAND +20% (was +10%) in 1Q26. From there on, we continue to forecast DRAM to remain undersupplied until 1Q27, and NAND 3Q26. We see the ongoing upside in conventional memory pricing as the main stock driver for Samsung. At 1.43x NTM book, we believe the stock is not yet discounting the strength and length of the upcycle ahead.

HBM shipments to catch up in 2026E

While we maintain our 2026 DRAM bit growth forecast of 15% YoY, we could see up to 2 pct pts upside depending on production yields / efficiency / mix. We continue to forecast HBM shipments to reach 7.5bn Gb in 2026, up 77% YoY. We continue to expect Samsung to provide HBM4 samples to Nvidia by February, which could lead to qualification by 2Q26 (with production starting earlier in 1Q). We believe Samsung remains first source for HBM for AMD and Open AI. Regarding Google, we believe Samsung is second source for TPU 7p, while Micron may be second source for TPU 7e (first source in both cases being SK Hynix).

Increasing forecasts well ahead of consensus on DDR/NAND ASP estimates

We increase our 4Q25 OP forecast to Won18.1tn from Won15.0tn (VA consensus: Won15.3tn) on the back of increased DRAM and NAND ASPs. We raise 2026E/27E OP to Won135.3tn/Won143.6tn (from Won101.2tn/Won109.5tn respectively), well ahead of consensus Won86.9tn/Won109.6tn respectively, and lift our 2026/27 EPS forecasts by 31%/29%. These changes are due to raised DDR/NAND ASPs as well as DRAM bit growth forecasts, which more than offset us lowering smartphone margins due to rising memory prices.

Valuation: lift price target to Won154,000 from Won128,000 – Buy

We value Samsung ordinary shares at 1.97x NTM book (was 1.79x) considering our 2026-30 average ROE estimate of 16.3% (was 14.6%) and CoE of 8.3% (was 8.2%). We also raise our Samsung GDR PT to US$2,610, from US$2,230, with the latest FX.

We've shown readers DDR5 DRAM pricing via DRAMeXchange…

Update: two months later https://t.co/Q4TPIrpzxV pic.twitter.com/O3KTKxZOVE

— zerohedge (@zerohedge) December 22, 2025

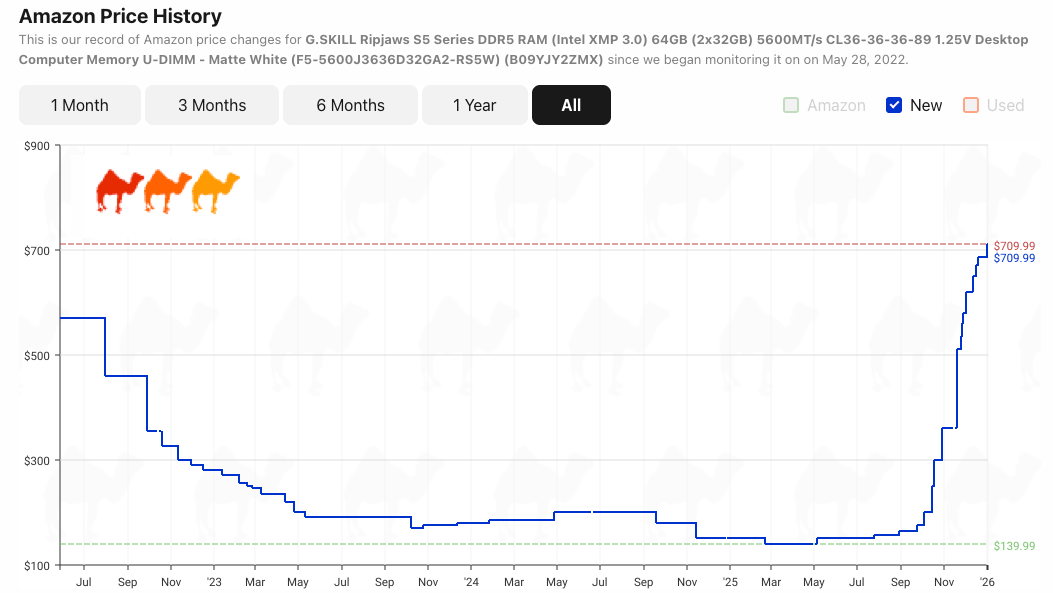

But now, take a look at DDR5 DRAM pricing on Amazon!

As a reminder, AI workloads are built around memory.

ZeroHedge Pro Subs can view the full note in the usual place, which includes a thesis map of the memory cycle.

Tyler Durden

Fri, 01/02/2026 – 12:40